This is “Income and Expenses”, section 2.1 from the book Individual Finance (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

2.1 Income and Expenses

Learning Objectives

- Identify and compare the sources and uses of income.

- Define and illustrate the budget balances that result from the uses of income.

- Outline the remedies for budget deficits and surpluses.

- Define opportunity and sunk costs and discuss their effects on financial decision making.

Personal finance is the process of paying for or financing a life and a way of living. Just as a business must be financed—its buildings, equipment, use of labor and materials, and operating costs must be paid for—so must a person’s possessions and living expenses. Just as a business relies on its revenues from selling goods or services to finance its costs, so a person relies on income earned from selling labor or capital to finance costs. You need to understand this financing process and the terms used to describe it. In the next chapter, you’ll look at how to account for it.

Where Does Income Come From?

IncomeEarnings of a given period. In the case of an indivdual or household, this is generally cash from wages, interest, dividends, or assets (such as rental income from real estate) that can be used for consumption or saved. is what is earned or received in a given period. There are various terms for income because there are various ways of earning income. Income from employment or self-employment is wages or salary. Deposit accounts, like savings accounts, earn interest, which could also come from lending. Owning stock entitles the shareholder to a dividend, if there is one. Owning a piece of a partnership or a privately held corporation entitles one to a draw.

The two fundamental ways of earning income in a market-based economy are by selling labor or selling capital. Selling labor means working, either for someone else or for yourself. Income comes in the form of a paycheck. Total compensation may include other benefits, such as retirement contributions, health insurance, or life insurance. Labor is sold in the labor market.

Figure 2.1

© 2010 Jupiterimages Corporation

Selling capital means investing: taking excess cash and selling it or renting it to someone who needs liquidityNearness to cash, or how easily and cheaply—with low transaction costs—an asset can be turned into cash. (access to cash). Lending is renting out capital; the interest is the rent. You can lend privately by direct arrangement with a borrower, or you can lend through a public debt exchange by buying corporate, government, or government agency bonds. Investing in or buying corporate stock is an example of selling capital in exchange for a share of the company’s future value.

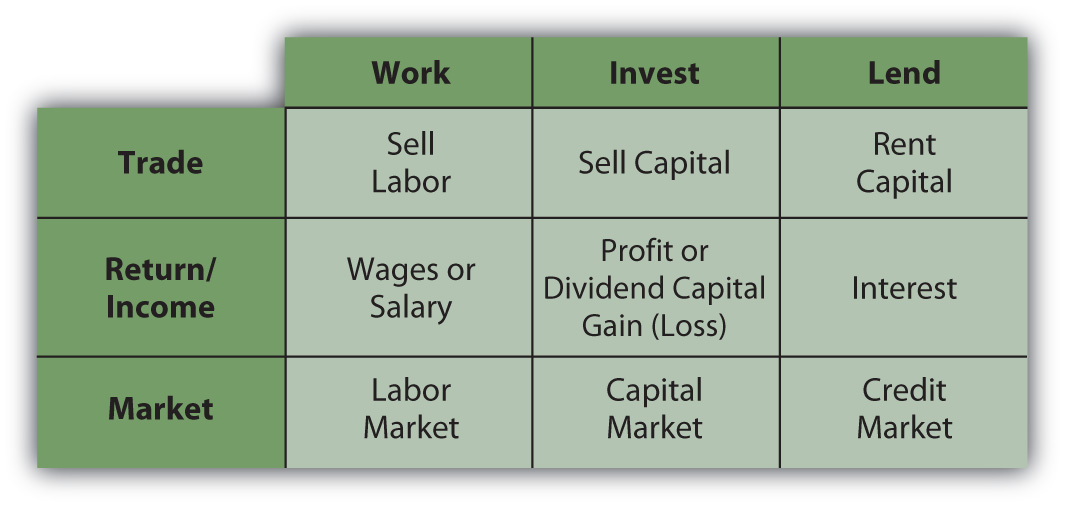

You can invest in many other kinds of assets, like antiques, art, coins, land, or commodities such as soybeans, live cattle, platinum, or light crude oil. The principle is the same: investing is renting capital or selling it for an asset that can be resold later, or that can create future income, or both. Capital is sold in the capital market and lent in the credit market—a specific part of the capital market (just like the dairy section is a specific part of the supermarket). Figure 2.2 "Sources of Income" shows the sources of income.

Figure 2.2 Sources of Income

In the labor market, the price of labor is the wage that an employer (buyer of labor) is willing to pay to the employee (seller of labor). For any given job, that price is determined by many factors. The nature of the work defines the education and skills required, and the price may reflect other factors as well, such as the status or desirability of the job.

In turn, the skills needed and the attractiveness of the work determine the supply of labor for that particular job—the number of people who could and would want to do the job. If the supply of labor is greater than the demand, if there are more people to work at a job than are needed, then employers will have more hiring choices. That labor market is a buyers’ market, and the buyers can hire labor at lower prices. If there are fewer people willing and able to do a job than there are jobs, then that labor market is a sellers’ market, and workers can sell their labor at higher prices.

Similarly, the fewer skills required for the job, the more people there will be who are able to do it, creating a buyers’ market. The more skills required for a job, the fewer people there will be to do it, and the more leverage or advantage the seller has in negotiating a price. People pursue education to make themselves more highly skilled and therefore able to compete in a sellers’ labor market.

When you are starting your career, you are usually in a buyers’ market (unless you have some unusual gift or talent), if only because of your lack of experience. As your career progresses, you have more, and perhaps more varied, experience and presumably more skills, and so can sell your labor in more of a sellers’ market. You may change careers or jobs more than once, but you would hope to be doing so to your advantage, that is, always to be gaining bargaining power in the labor market.

Many people love their work for many reasons other than the pay, however, and choose it for those rewards. Labor is more than a source of income; it is also a source of many intellectual, social, and other personal gratifications. Your labor nevertheless is also a tradable commodity and has a market value. The personal rewards of your work may ultimately determine your choices, but you should be aware of the market value of those choices as you make them.

Your ability to sell labor and earn income reflects your situation in your labor market. Earlier in your career, you can expect to earn less than you will as your career progresses. Most people would like to reach a point where they don’t have to sell labor at all. They hope to retire someday and pursue other hobbies or interests. They can retire if they have alternative sources of income—if they can earn income from savings and from selling capital.

Capital markets exist so that buyers can buy capital. Businesses always need capital and have limited ways of raising it. Sellers and lenders (investors), on the other hand, have many more choices of how to invest their excess cash in the capital and credit markets, so those markets are much more like sellers’ markets. The following are examples of ways to invest in the capital and credit markets:

- Buying stocks

- Buying government or corporate bonds

- Lending a mortgage

The market for any particular investment or asset may be a sellers’ or buyers’ market at any particular time, depending on economic conditions. For example, the market for real estate, modern art, sports memorabilia, or vintage cars can be a buyers’ market if there are more sellers than buyers. Typically, however, there is as much or more demand for capital as there is supply. The more capital you have to sell, the more ways you can sell it to more kinds of buyers, and the more those buyers may be willing to pay. At first, however, for most people, selling labor is their only practical source of income.

Where Does Income Go?

ExpensesThe costs of consumption or daily living. are costs for items or resources that are used up or consumed in the course of daily living. Expenses recur (i.e., they happen over and over again) because food, housing, clothing, energy, and so on are used up on a daily basis.

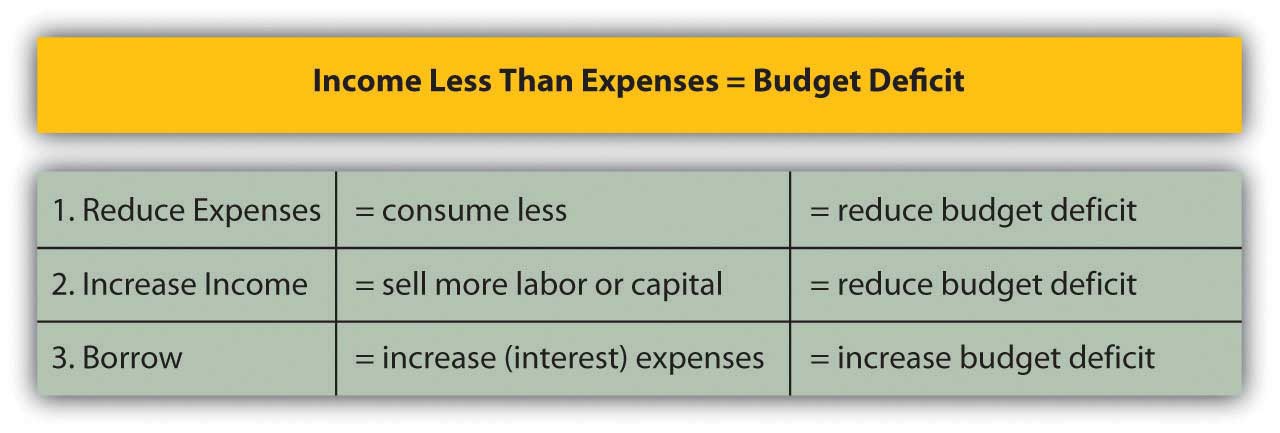

When income is less than expenses, you have a budget deficitA shortfall of available funds created when income is less than the expenses.—too little cash to provide for your wants or needs. A budget deficit is not sustainable; it is not financially viable. The only choices are to eliminate the deficit by (1) increasing income, (2) reducing expenses, or (3) borrowing to make up the difference. Borrowing may seem like the easiest and quickest solution, but borrowing also increases expenses, because it creates an additional expense: interest. Unless income can also be increased, borrowing to cover a deficit will only increase it.

Better, although usually harder, choices are to increase income or decrease expenses. Figure 2.3 "Budget Deficit" shows the choices created by a budget deficit.

Figure 2.3 Budget Deficit

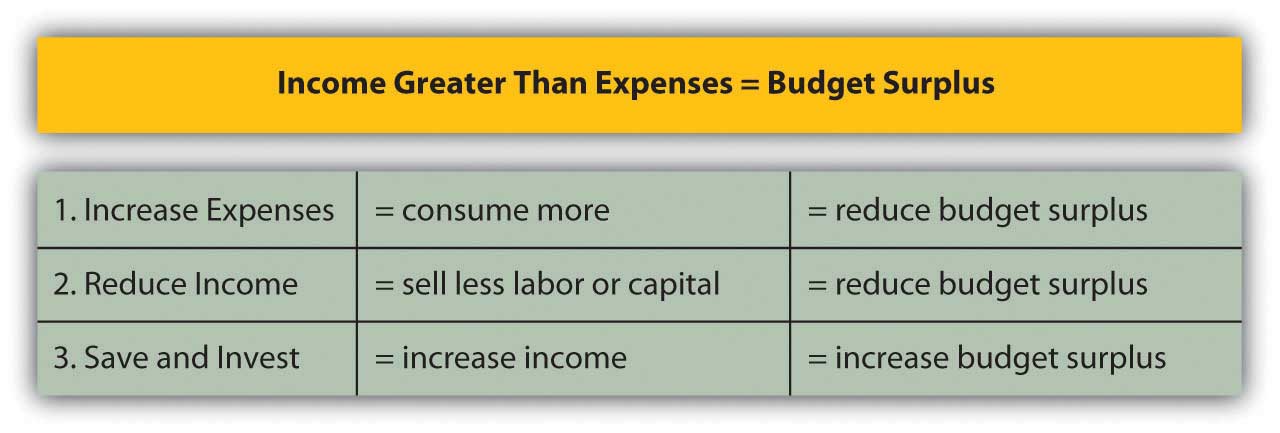

When income for a period is greater than expenses, there is a budget surplusAn excess of available funds created when income is greater than the expenses.. That situation is sustainable and remains financially viable. You could choose to decrease income by, say, working less. More likely, you would use the surplus in one of two ways: consume more or save it. If consumed, the income is gone, although presumably you enjoyed it.

If saved, however, the income can be stored, perhaps in a piggy bank or cookie jar, and used later. A more profitable way to save is to invest it in some way—deposit in a bank account, lend it with interest, or trade it for an asset, such as a stock or a bond or real estate. Those ways of saving are ways of selling your excess capital in the capital markets to increase your wealth. The following are examples of savings:

- Depositing into a statement savings account at a bank

- Contributing to a retirement account

- Purchasing a certificate of deposit (CD)

- Purchasing a government savings bond

- Depositing into a money market account

Figure 2.4

© 2010 Jupiterimages Corporation

Figure 2.5 "Budget Surplus" shows the choices created by a budget surplus.

Figure 2.5 Budget Surplus

Opportunity Costs and Sunk Costs

There are two other important kinds of costs aside from expenses that affect your financial life. Suppose you can afford a new jacket or new boots, but not both, because your resources—the income you can use to buy clothing—are limited. If you buy the jacket, you cannot also buy the boots. Not getting the boots is an opportunity costThe cost of sacrificing the next best choice because of the choice made; the value of the next best choice, which is forgone once a choice is made. of buying the jacket; it is cost of sacrificing your next best choice.

In personal finance, there is always an opportunity cost. You always want to make a choice that will create more value than cost, and so you always want the opportunity cost to be less than the benefit from trade. You bought the jacket instead of the boots because you decided that having the jacket would bring more benefit than the cost of not having the boots. You believed your benefit would be greater than your opportunity cost.

In personal finance, opportunity costs affect not only consumption decisions but also financing decisions, such as whether to borrow or to pay cash. Borrowing has obvious costs, whereas paying with your own cash or savings seems costless. Using your cash does have an opportunity cost, however. You lose whatever interest you may have had on your savings, and you lose liquidity—that is, if you need cash for something else, like a better choice or an emergency, you no longer have it and may even have to borrow it at a higher cost.

When buyers and sellers make choices, they weigh opportunity costs, and sometimes regret them, especially when the benefits from trade are disappointing. Regret can color future choices. Sometimes regret can keep us from recognizing sunk costsCosts that have been incurred in past transactions and cannot be recovered..

Sunk costs are costs that have already been spent; that is, whatever resources you traded are gone, and there is no way to recover them. Decisions, by definition, can be made only about the future, not about the past. A trade, when it’s over, is over and done, so recognizing that sunk costs are truly sunk can help you make better decisions.

For example, the money you spent on your jacket is a sunk cost. If it snows next week and you decide you really do need boots, too, that money is gone, and you cannot use it to buy boots. If you really want the boots, you will have to find another way to pay for them.

Unlike a price tag, opportunity cost is not obvious. You tend to focus on what you are getting in the trade, not on what you are not getting. This tendency is a cheerful aspect of human nature, but it can be a weakness in the kind of strategic decision making that is so essential in financial planning. Human nature also may make you focus too much on sunk costs, but all the relish or regret in the world cannot change past decisions. Learning to recognize sunk costs is important in making good financial decisions.

Key Takeaways

- It is important to understand the sources (incomes) and uses (expenses) of funds, and the budget deficit or budget surplus that may result.

- Wages or salary is income from employment or self-employment; interest is earned by lending; a dividend is the income from owning corporate stock; and a draw is income from a partnership.

- Deficits or surpluses need to be addressed, and that means making decisions about what to do with them.

- Increasing income, reducing expenses, and borrowing are three ways to deal with budget deficits.

- Spending more, saving, and investing are three ways to deal with budget surpluses.

- Opportunity costs and sunk costs are hidden expenses that affect financial decision making.

Exercises

- Where does your income come from, and where does it go? Analyze your inflows of income from all sources and outgoes of income through expenditures in a month, quarter, or year. After analyzing your numbers and converting them to percentages, show your results in two figures, using proportions of a dollar bill to show where your income comes from and proportions of another dollar bill to show how you spend your income. How would you like your income to change? How would you like your distribution of expenses to change? Use your investigation to develop a rough personal budget.

- Examine your budget and distinguish between wants and needs. How do you define a financial need? What are your fixed expenses, or costs you must pay regularly each week, month, or year? Which of your budget categories must you provide for first before satisfying others? To what extent is each of your expenses discretionary—under your control in terms of spending more or less for that item or resource? Which of your expenses could you reduce if you had to or wanted to for any reason?

- If you had a budget deficit, what could you do about it? What would be the best solution for the long term? If you had a budget surplus, what could you do about it? What would be your best choice, and why?

- You need a jacket, boots, and gloves, but the jacket you want will use up all the money you have available for outerwear. What is your opportunity cost if you buy the jacket? What is your sunk cost if you buy the jacket? How could you modify your consumption to reduce opportunity cost? If you buy the jacket but find that you need the boots and gloves, how could you modify your budget to compensate for your sunk cost?