This is “Structure and Analysis of Insurance Contracts”, chapter 10 from the book Enterprise and Individual Risk Management (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

Chapter 10 Structure and Analysis of Insurance Contracts

As discussed in Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts", an insurance policy is a contractual agreement subject to rules governing contracts. Understanding those rules is necessary for comprehending an insurance policy. It is not enough, however. We will be spending quite a bit of time in the following chapters discussing the specific provisions of various insurance contracts. These provisions add substance to the general rules of contracts already presented and should give you the skills needed to comprehend any policy.

In Chapter 10 "Structure and Analysis of Insurance Contracts", we offer a general framework of insurance contracts, called policies. Because most policies are somewhat standardized, it is possible to present a framework applicable to almost all insurance contracts. As an analogy, think about grammar. In most cases, you can follow the rules almost implicitly, except when you have exceptions to the rules. Similarly, insurance policies follow comparable rules in most cases. Knowing the format and general content of insurance policies will help later in understanding the specific details of each type of coverage for each distinct risk. This chapter covers the following:

- Links

- Entering into the contract: applications, binders, and conditional and binding receipts

- The contract: declarations, insuring clauses, exclusions and exceptions, conditions, and endorsements and riders

Links

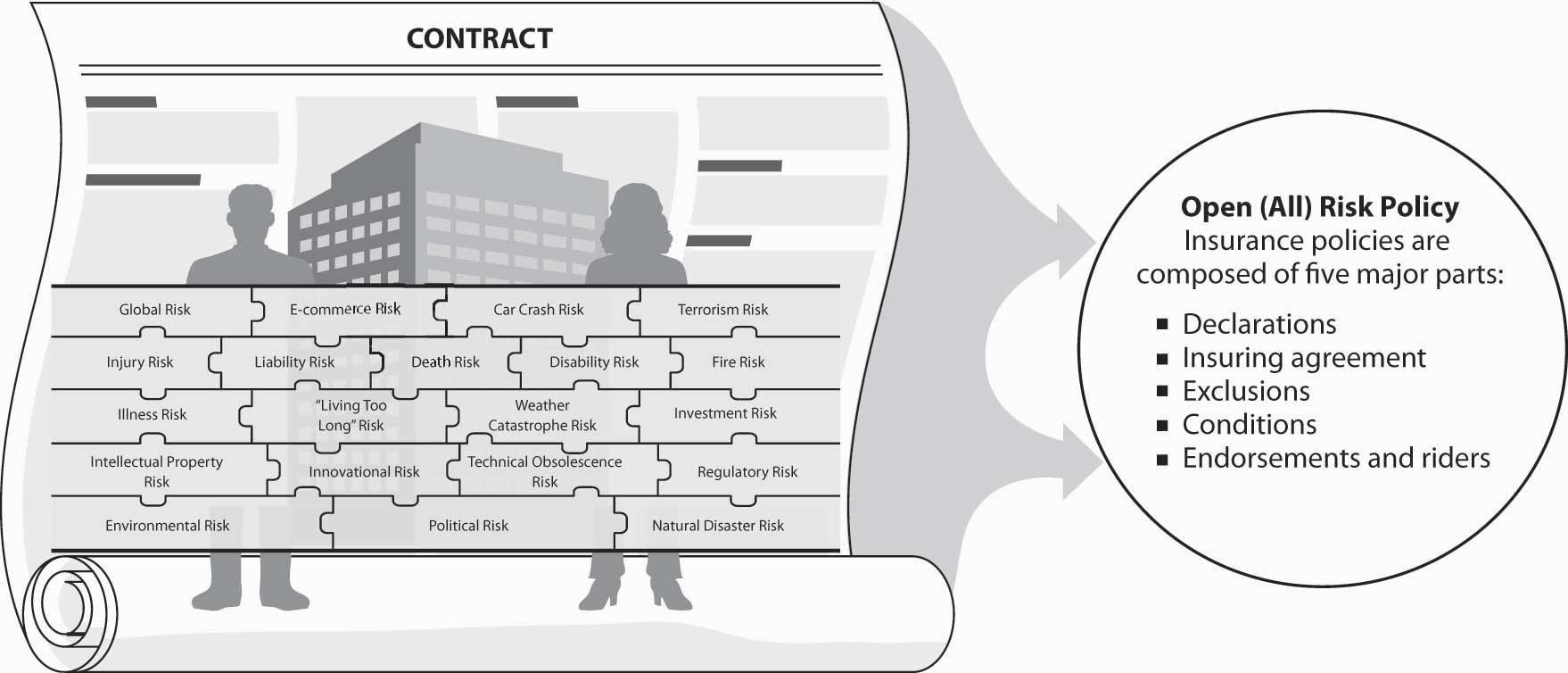

By now, we assume you are accustomed to connecting the specific topics of each chapter to the big picture of your holistic risk. This chapter is wider in scope. We are not yet delving into the specifics of each risk and its insurance programs. However, compared with Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts", we are drilling down a step further into the world of insurance legal documents. We focus on the open-peril type of policy, which covers all risks. This means that everything is covered unless specifically excluded, as shown in Figure 10.1 "Links between the Holistic Risk Puzzle and the Insurance Contract". Nevertheless, the open-peril policy has many exclusions and more are added as new risks appear on the horizon. For the student who is first introduced to this field, this unique element is an important one to understand. Most insurance contracts in use today do not list the risks that are covered; rather, the policy lets you know that everything is covered, even new, unanticipated risks such as anthrax (described in the box “How to Handle the Risk Management of a Low-Frequency but Scary Risk Exposure: The Anthrax Scare?” in Chapter 4 "Evolving Risk Management: Fundamental Tools"). When the industry realizes that a new peril is too catastrophic, it then exerts efforts to exclude such risks from the standardized, regulated policies. Such efforts are not easy and are met with resistance in many cases. As you learned in Chapter 6 "The Insurance Solution and Institutions", catastrophic risks are not insurable by private insurers; therefore, they are excluded from the policies. In 2005, the topic of wind versus water was of concern as a result of hurricanes Katrina and Rita. Despite the devastation, all damages caused by flood water were excluded from the policies because floods are considered catastrophic. Another case in point is the terrorism exclusion that became moot after President Bush signed the Terrorism Risk Insurance Act (TRIA) in 2002.

Figure 10.1 Links between the Holistic Risk Puzzle and the Insurance Contract

Another important element achieved by exclusions, in addition to excluding the uninsurable risk of catastrophes, is duplication of coverage. Each policy is designed not to overlap with another policy. Such duplication would violate the contract of indemnity principal of insurance contracts. The homeowner’s liability coverage excludes automobile liability, workers’ compensation liability, and other such exposures that are nonstandard to home and personal activities. These specifics will be discussed in later chapters, but for now, it is important to emphasize that exclusions are used to reduce the moral hazard of allowing insureds to be paid twice for the same loss.

Thus, while each insurance policy has the components outlined in Figure 10.1 "Links between the Holistic Risk Puzzle and the Insurance Contract", the exclusions are the part that requires in-depth study. Exclusions within exclusions in some policies are like a maze. We not only must ensure that we are covered for each risk in our holistic risk picture, we must also make sure no areas are left uncovered by exclusions. At this point, you should begin to appreciate the complexity of putting the risk management puzzle together to ensure completeness.

10.1 Entering into the Contract

Learning Objectives

In this section we elaborate on the following:

- The preliminary steps of entering into an insurance contract

- The roles assumed by applications and binders in the offer and acceptance process

You may recall from Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts" that every contract requires an offer and an acceptance. This is also true for insurance. The offer and acceptance occur through the application process.

Applications

Although more insurance is sold rather than bought, the insured is still required to make an applicationAn offer to buy insurance, which is an offer to buy insurance. The function of the agent is to induce a potential insured to make an offer. As a practical matter, the agent also fills out the application and then asks for a signature after careful study of the application. The application identifies the insured in more or less detail, depending on the type of insurance. It also provides information about the exposure involved.

For example, in an application for an automobile policy, you would identify yourself; describe the automobile to be insured; and indicate the use of the automobile, where it will be garaged, who will drive it, and other facts that help the insurer assess the degree of risk you represent as a policyholder. Some applications for automobile insurance also require considerable information about your driving and claim experience, as well as information about others who may use the car. In many cases, such as life insurance, the written application becomes part of the policy. Occasionally, before an oral or written property/casualty application is processed into a policy, a temporary contract, or binder, may be issued.

Binders

As discussed in Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts", property/casualty insurance coverage may be provided while the application is being processed. This is done through the use of a binder, which is a temporary contract to provide coverage until the policy is issued by the agent or the company.

In property/casualty insurance, an agent who has binding authority can create a contract between the insurance company and the insured. Two factors influence the granting of such authority. First, some companies prefer to have underwriting decisions made by specialists in the underwriting department, so they do not grant binding authority to the agent. Second, some policies are cancelable; others are not. The underwriting errors of an agent with binding authority may be corrected by cancellation if the policy is cancelable. Even with cancelable policies, the insurer is responsible under a binder for losses that occur prior to cancellation. If it is not cancelable, the insurer is obligated for the term of the contract.

The binder may be written or oral. For example, if you telephone an agent and ask to have your house insured, the agent will ask for the necessary information, give a brief statement about the contract—the coverage and the premium cost—and then probably say, “You are covered.” At this point, you have made an oral application and the agent has accepted your offer by creating an oral binder. The agent may mail or e-mail a written binder to you to serve as evidence of the contract until the policy is received. The written binder shows who is insured, for what perils, the amount of the insurance, and the company with which coverage is placed.

In most states, an oral binder is as legal as a written one, but in case of a dispute it may be difficult to prove its terms. Suppose your house burns after the oral binder has been made but before the policy has been issued, and the agent denies the existence of the contract. How can you prove there was a contract? Or suppose the agent orally binds the coverage, a fire occurs, and the agent dies before the policy is issued. Unless there is evidence in writing, how can you prove the existence of a contract? Suppose the agent does not die and does not deny the existence of the contract, but has no evidence in writing. If the agent represents only one company, he or she may assert that the company was bound and the insured can collect for the loss. But what if the agent represents more than one company? Which one is bound? Typically, the courts will seek a method to allocate liability according to the agent’s common method of distributing business. Or if that is not determinable, relevant losses might be apportioned among the companies equally. Most agents, however, keep records of their communication with insureds, including who is to provide coverage.

Conditional and Binding Receipts

Conditional and binding receipts in life insurance are somewhat similar to the binders in property/casualty insurance but contain important differences. If you pay the first premium for a life insurance policy at the time you sign the application, the agent typically will give you either a conditional receipt or a binding receipt. The conditional receiptPolicy that does not bind the coverage of life insurance at the time it is issued, but it does put the coverage into effect retroactive to the time of application if one meets all the requirements for insurability as of the date of the application. does not bind the coverage of life insurance at the time it is issued, but it does put the coverage into effect retroactive to the time of application if one meets all the requirements for insurability as of the date of the application. A claim for benefits because of death prior to issuance of the policy generally will be honored, but only if you were insurable when you applied. Some conditional receipts, however, require the insured to be in good health when the policy is delivered.

In contrast, a claim for the death benefit under a binding receiptPolicy that will be paid if death occurs while one’s application for life insurance is being processed, even if the deceased is found not to be insurable. will be paid if death occurs while one’s application for life insurance is being processed even if the deceased is found not to be insurable. Thus, the binding receipt provides interim coverage while your application is being processed, whether or not you are insurable. This circumstance parallels the protection provided by a binder in property/casualty insurance.In a few states, the conditional receipt is construed to be the same as the binding receipt. See William F. Meyer, Life and Health Insurance Law: A Summary, 2nd ed. (Cincinnati: International Claim Association, 1990), 196–217.

Key Takeaways

In this section you studied that the act of entering into an insurance contract, like all contracts, requires offer and acceptance between two parties:

- The insurance application serves as the insured’s offer to buy insurance.

- An agent may accept an application through oral or written binder in property/casualty insurance and through conditional receipt or a binding receipt in life/health insurance

Discussion Questions

- What is the difference between a conditional receipt and a binding receipt?

- You apply for homeowners insurance and are issued a written binder. Before your application has been finalized, your house burns down in an accidental fire. Are you covered for this loss? What about in the case of an oral binder?

- Dave was just at his insurance agent’s office applying for health insurance. On his way home from the agent’s office, Dave had a serious accident that kept him hospitalized for two weeks. Would the health insurance policy Dave just applied for provide coverage for this hospital expense?

10.2 The Contract

Learning Objectives

In this section we elaborate on the following major elements of insurance contracts:

- Declarations

- Insuring agreement

- Exclusions

- Conditions

- Endorsements and riders

Having completed the offer and the acceptance and met the other requirements for a contract, a contract now exists. What does it look like? Insurance policies are composed of five major parts:

- Declarations

- Insuring agreement

- Exclusions

- Conditions

- Endorsements and riders

These parts typically are identified in the policy by headings. (A section titled “definition” is also becoming common.) Sometimes, however, they are not so prominently displayed, and it is much more common to have explicit section designations in property/casualty contracts than it is in life/health contracts. Their general intent and nature, however, has the same effect.

Declarations

Generally, the declarations section is the first part of the insurance policy. Some policies, however, have a cover (or jacket) ahead of the declarations. The cover identifies the insurer and the type of policy.

DeclarationsStatements that identify the person(s) or organization(s) covered by a contract, give information about the loss exposure, and provide the basis upon which the contract is issued and the premium determined. are statements that identify the person(s) or organization(s) covered by the contract, give information about the loss exposure, and provide the basis upon which the contract is issued and the premium determined. This information may be obtained orally or in a written application. The declarations section may also include the period of coverage and limitations of liability. (The latter may also appear in other parts of the contract.)

Period of Coverage

All insurance policies specify the period of coverageThe time duration for which coverage applies., or the time duration for which coverage applies. Life and health policies may provide coverage for the entire life of the insured, a specified period of years, or up until a specified age. Health policies and term life policies often cover a year at a time. Most property insurance policies are for one year or less (although longer policies are available). Perpetual policies remain in force until canceled by you or the insurer. Liability policies may be for a three-month or six-month period, but most are for a year. Some forms of automobile insurance may be written on a continuous basis, with premiums payable at specified intervals, such as every six months. Such policies remain in force as long as premiums are paid or until they are canceled. Whatever the term during which any policy is to be in force, it will be carefully spelled out in the contract. During periods when insureds may expect a turn to hard markets in the underwriting cycles, they may want to fix the level of premiums for a longer period and will sign contracts for longer than one year, such as three years.

Limitations of Liability

All insurance policies have clauses that place limitations of liabilityThe maximum amount payable by an insurance policy. (maximum amount payable by the insurance policy) on the insurer. Life policies promise to pay the face amount of the policy. Health policies typically limit payment to a specified amount for total medical expenses during one’s lifetime and have internal limits on the payment of specific services, such as a surgical procedure. Property insurance policies specify as limits actual cash value or replacement value, insurable interest, cost to repair or replace, and the face amount of insurance. Limits exist in liability policies for the amount payable per claim, sometimes per injured claimant, sometimes per year, and sometimes per event. Remember the example in Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts" of the dispute between the leaseholder and the insurer over the number of events in the collapse of the World Trade Center (WTC) on September 11, 2001. The dispute was whether the attack on the WTC constituted two events or one. Defense services, provided in most liability policies, are limited only to the extent that litigation falls within coverage terms and the policy proceeds have not been exhausted in paying judgments or settlements. Because of the high cost of providing legal defense in recent years, however, attempts to limit insurer responsibility to some dollar amount have been made.

Retained Losses

In many situations, it is appropriate not to transfer all of an insured’s financial interest in a potential loss. Loss retention benefits the insured when losses are predictable and manageable. For the insurer, some losses are better left with the insured because of moral hazard concerns. Thus, an insured might retain a portion of covered losses through a variety of policy provisions. Some such provisions are deductibles, coinsurance in property insurance, copayments in health insurance, and waiting periods in disability insurance. Each is discussed at some length in later chapters. For now, realize that the existence of such provisions typically is noted in the declarations section of the policy.

Insuring Clauses

The second major element of an insurance contract, the insuring clauseA general statement of the promises the insurer makes to the insured. or agreement, is a general statement of the promises the insurer makes to the insured. Insuring clauses may vary greatly from policy to policy. Most, however, specify the perils and exposures covered, or at least some indication of what they might be.

Variation in Insuring Clauses

Some policies have relatively simple insuring clauses, such as a life insurance policy, which could simply say, “The company agrees, subject to the terms and conditions of this policy, to pay the amount shown on page 2 to the beneficiary upon receipt at its Home Office of proof of the death of the insured.” Package policies are likely to have several insuring clauses, one for each major type of coverage and each accompanied by definitions, exclusions, and conditions. An example of this type is the personal automobile policy, described in Chapter 1 "The Nature of Risk: Losses and Opportunities".

Some insuring clauses are designated as the “insuring agreement,” while others are hidden among policy provisions. Somewhere in the policy, however, it states that the “insurer promises to pay….” This general description of the insurer’s promises is the essence of an insuring clause.

Open-Perils versus Named-Perils

The insuring agreement provides a general description of the circumstances under which the policy becomes applicable. The circumstances include the covered loss-causing events, called perilsThe causes of loss.. They may be specified in one of two ways.

A named-perils policyPolicy that covers only losses caused by the perils listed in the policy. covers only losses caused by the perils listed in the policy. If a peril is not listed, loss resulting from it is not covered. For example, one form of the homeowner’s policy, HO-2, insures for direct loss to the dwelling, other structures, and personal property caused by eighteen different perils. Only losses caused by these perils are covered. Riot or civil commotion is listed, so a loss caused by either is covered. On the other hand, earthquake is not listed, so a loss caused by earthquake is not covered.

An open-perils policyPolicy that covers losses caused by all perils except those excluded. (formerly called “all risk”) covers losses caused by all perils except those excluded. This type of policy is most popular in property policies. It is important to understand the nature of such a policy because the insured has to look for what is not covered rather than what is covered. The exclusions in an open-perils policy are more definitive of coverage than in a named-perils policy. Generally, an open-perils policy provides broader coverage than a named-perils policy, although it is conceivable, if unlikely, that an open-perils policy would have such a long list of exclusions that the coverage would be narrower.

As noted in the Links section, many exclusions in property policies have been in the limelight. After September 11, 2001, the terrorism exclusion was the first added exclusion to all commercial policies but was rescinded after the enactment of TRIA in 2002 and its extensions. The mold exclusion was another new exclusion of our age. The one old exclusion that received major attention in 2005 in the wake of hurricanes Katrina and Rita is the flood exclusion in property policies. Flood coverage is provided by the federal government and is limited in its scope (see Chapter 1 "The Nature of Risk: Losses and Opportunities"). Additional exclusions will be discussed further in Chapter 11 "Property Risk Management" and Chapter 12 "The Liability Risk Management". In the 1980s, pollution liability was excluded after major losses. As noted in Chapter 6 "The Insurance Solution and Institutions", most catastrophes would be excluded because they are not considered insurable by private insurers. A most common exclusion, as noted above, is the war exclusion. The insurance industry decided not to trigger this exclusion in the aftermath of September 11. For a closer look, see the box below, Note 10.15 "The Risk of War".

Policies written on a named-perils basis cannot cover all possible causes of loss because of “unknown peril.” There is always the possibility of loss caused by a peril that was not known to exist and so was not listed in the policy. For this reason, open-perils policies cover many perils not covered by named-perils policies. This broader coverage usually requires a higher premium than a named-perils policy, but it is often preferable because it is less likely to leave gaps in coverage. The anthrax scare described in Chapter 4 "Evolving Risk Management: Fundamental Tools" is an example of an unknown peril that was covered by the insurance industry’s policies.

Very few, if any, policies are “all risk” in the sense of covering every conceivable peril. Probably the closest approach to such a policy in the property insurance field is the comprehensive glass policy, which insures against all glass breakage except those caused by fire, war, or nuclear peril. Most life insurance policies cover all perils except for suicide during the first year or the first two years. Health insurance policies often are written on an open-perils basis, covering medical expenses from any cause not intentional. Some policies, however, are designed to cover specific perils such as cancer (discussed in Chapter 2 "Risk Measurement and Metrics"). Limited-perils policies are popular because many people fear the consequences of certain illnesses. Of course, the insured is well-advised to be concerned with (protect against) the loss, regardless of the cause.

The Risk of War

“This means war!” was a frequent refrain among angry Americans in the days after September 11, 2001. Even President George W. Bush repeatedly referred to the terrorist attacks on the World Trade Center and the Pentagon as an “act of war.” One politician who disagreed with that choice of words was Representative Michael Oxley.

By definition and by U.S. law, war is an act of violent conflict between two nations. The hijackers, it was soon determined, were working not on behalf of any government but for the al Qaeda network of terrorists. Thus, a week after the attacks, Oxley, chairperson of the Financial Services Committee of the U.S. House of Representatives, sent a letter to the National Association of Insurance Commissioners urging the insurance industry not to invoke war risk exclusions to deny September 11 claims.

Most insurers had already come to the same conclusion. Generally, auto, homeowner’s, commercial property, business interruption, and (in some states) worker’s compensation policies contain act-of-war exclusions, meaning that insurance companies can refuse to pay claims arising from a war or a warlike act. To illustrate, the standard commercial property policy form provided by the Insurance Services Office contains the following exclusions:

- War, including undeclared or civil war

- Warlike action by a military force, including action in hindering or defending against an actual or expected attack, by any government, sovereign or other authority using military personnel or other agents

- Insurrection, rebellion, revolution, usurped power, or action taken by governmental authority in hindering or defending against any of these

Wars are not considered insurable events: they are unpredictable, intentional, and potentially catastrophic. (Recall the discussion in Chapter 6 "The Insurance Solution and Institutions" on insurable and uninsurable risks.) The risks of war are simply too great for an insurance company to accept.

The war exclusion clause has given rise to few lawsuits, but in each case the courts have supported its application “only in situations involving damage arising from a genuine warlike act between sovereign entities.” Pan American World Airways v. Aetna Casualty and Surety Co., 505 F2d 989 (1974), involved coverage for the hijacking and destruction of a commercial aircraft. The Second Circuit Court of Appeals held that the hijackers, members of the Popular Front for the Liberation of Palestine, were not “representatives of a government,” and thus the war exclusion did not apply. The insurers were liable for the loss. A war exclusion claim denial was upheld in TRT/FTC Communications, Inc. v. Insurance Company of the State of Pennsylvania, 847 F. Supp. 28 (Del. Dist. 1993), because the loss occurred in the context of a declared war between the United States and Panama—two sovereign nations.

With some $50 billion at stake from the September 11 attacks, it wouldn’t have been surprising if some insurers considered taking a chance at invoking the war exclusion clause. Instead, companies large and small were quick to announce that they planned to pay claims fairly and promptly. “We have decided that we will consider the events of September 11 to be ‘acts of terrorism,’ not ‘acts of war,’” said Peter Bruce, Senior Executive Vice President of Northwestern Mutual Life Insurance. The industry agreed.

Sources: “Insurers: WTC Attack Not Act of War,” Insurance-Letter, September 17, 2001, http://www.cybersure.com/godoc/1872.htm; Jack P. Gibson et al., “Attack on America: The Insurance Coverage Issues,” International Risk Management Institute, Inc., September 2001, http://www.imri.com; Tim Reason, “Acts of God and Monsters No Longer Covered: Insurers Say Future Policies Will Definitely Exclude Terrorist Attacks,” CFO.com, November 19, 2001, http://www.cfo.com/article/1,5309,5802%7C%7CA%7C736%7C8,00.html; Susan Massmann, “Legal Background Outlined for War Risk Exclusion,” National Underwriter Online News Service, September 18, 2001; “Northwestern Mutual Won’t Invoke War Exclusion on Claims,” The (Milwaukee) Business Journal, September 14, 2001.

Exposures to Loss

Generally, the exposures to be covered are also defined (broadly speaking) in the insuring agreement. For example, the liability policy states that the insurer will pay “those sums the insured is legally obligated to pay for damages….” In addition, “the Company shall have the right and duty to defend….” The exposures in this situation are legal defense costs and liability judgments or settlements against the insured.

In defining the exposures, important information, such as the basis of valuation and types of losses covered, is needed. Various valuation methods have already been discussed. Actual cash value and replacement cost are the most common means of valuing property loss. Payments required of defendants, either through mutually acceptable settlements or court judgments, define the value of liability losses. The face value (amount of coverage) of a life insurance policy represents the value paid upon the insured’s death. Health insurance policies employ a number of valuation methods, including an amount per day in the hospital or per service provided, or—more likely—the lesser of the actual cost of the service or the customary and prevailing fee for this service. Health maintenance organizations promise the provision of services, as such, rather than a reimbursement of their cost.

The types of covered losses are also generally stated in the insuring agreement. Many property insurance policies, for example, cover only direct loss. Direct lossThe value of property that is physically destroyed or damaged, not including the loss caused by inability to use the property. to property is the value that is physically destroyed or damaged, not the loss caused by inability to use the property. Other policies that cover loss of use of property without physical damage to the property are called consequential or indirect lossA nonphysical loss such as loss of business.. In the aftermath of Hurricane Rita, many Texas coastal residents who evacuated encountered indirect loss without damage to their homes. This included the evacuation of Galveston and Houston. Coverage for these losses was disputed by insurers, such as Allstate, that tried to exclude these indirect losses. In addition, in the introduction to this chapter, it was explained how important the consequential loss coverage was to the businesses that suffered indirectly from the September 11 attacks. A report released by PricewaterhouseCoopers in New York City noted that business interruption claims came from a wide scope of industries, including financial services, communications, media, and travel industries, that were not in the attack zone.“9/11 Business Interruption Claims Analysis,” National Underwriter Online News Service, February 20, 2002. Many remote businesses were disrupted when the world transportation networks were paralyzed. It was estimated that losses up to $10 billion were caused by these indirect effects.Diana Reitz, “9/11 Spotlights Business Interruption Threat—What Is the Art and Science of Establishing the Accurate Limit of Coverage?” National Underwriter, Property/Casualty Edition, April 16, 2004, http://www.propertyandcasualtyinsurancenews.com/cms/NUPC/Weekly%20Issues/Issues/2004/15/p15911spotlights?searchfor= (accessed March 8, 2009).

Business interruptionLosses that occur when an organization is unable to sell its goods or services and/or unable to produce goods for sale because of direct or indirect loss. losses occur when an organization is unable to sell its goods or services, and/or unable to produce goods for sale because of direct or indirect loss. Generally, these losses are due to some property damage considered direct loss. Such lost revenues typically translate into lost profits. The 1992 Chicago flood, for example, required that Marshall Fields downtown store close its doors for several days while crews worked to clean up damage caused by the flood waters.In April 1992, part of Chicago’s underground tunnel system was flooded when the river pushed back a wall far enough to cause a rapid flow of water into the tunnels. Water levels rose high enough to damage stored property, force electrical supplies to be shut off, and cause concern about the stability of structures built above the tunnels. When loss is caused by property damage not owned by the business, it is considered a contingent business interruptionLoss caused by property damage not owned by the business.. If Marshall Fields reduced its orders to suppliers of its goods, for instance, those suppliers may experience contingent business interruption loss caused by the water damage, even though their own property was not damaged.

Alternatively, some organizations choose to continue operating following property damage, but they are able to do so only by incurring additional costs known as extra expense lossesAdditional costs incurred by organizations that choose to continue operating following property damage.. These costs also reduce profits. Continuing with the 1992 Chicago flood example, consider the various accounting firms who could not use their offices the second week in April. With the upcoming tax filing deadline, these firms chose to rent additional space in other locations so they could meet their clients’ needs. The additional rental expense (and other costs) resulted in reduced profits to the accounting firms. Yet a variety of service organizations, including accountants, insurance agents, and bankers, prefer to incur such expenses in order to maintain their reputation of reliability, upon which their long-term success and profits depend. Closing down, even temporarily, could badly hurt the organization.

Individuals and families too may experience costs associated with loss of use. For example, if your home is damaged, you may need to locate (and pay for) temporary housing. You may also incur abnormal expenses associated with the general privileges of home use, such as meals, entertainment, telephones, and similar conveniences. Likewise, if your car is unavailable following an accident, you must rent a car or spend time and money using other forms of transportation. Thus, while a family’s loss of use tends to focus on extra expense, its effect may be as severe as that of an organization.

Liability policies, on the other hand, may cover liability for property damage, bodily injury, personal injury, and/or punitive damages. Property damageLiability that includes responsibility both for the physical damage to property and the loss of use of property. liability includes responsibility both for the physical damage to property and the loss of use of property. Bodily injuryPhysical injury to a person, including the pain and suffering that may result. is the physical injury to a person, including the pain and suffering that may result. Personal injuryNonphysical injury to a person, including damage caused by libel, slander, false imprisonment, and the like. is the nonphysical injury to a person, including damage caused by libel, slander, false imprisonment, and the like. Punitive damagesAwards intended to punish an offender for exceptionally undesirable behavior. are damages assessed against defendants for gross negligence, supposedly for the purpose of punishment and to deter others from acting in a similar fashion. Examples of punitive damages in recent cases and their ethical implications are featured in the box “Are Punitive Damages out of Control?”

Are Punitive Damages out of Control?

In December 2005, a California jury delivered a guilty verdict and awarded $172 million in damages against Wal-Mart Stores, Inc., for not giving the appropriate lunch breaks to its thousands of employees. The verdict included $57.3 million in general damages and $115 million in punitive damages. Wal-Mart planned to appeal. In 2002, a California state court judge awarded $30 million against grocery chain Kroger, where six employees had been verbally harassed by a store manager. The verdict was reduced to a mere $8.25 million when the upper court decided it was “grossly excessive.” A jury in Laredo, Texas, awarded $108 million to Mexican heiress Cristina Brittingham Sada de Ayala in a lawsuit against her stepmother for failing to repay a $34 million loan. A Utah jury ordered State Farm to pay a policyholder $145 million in punitive damages for handling a claim in bad faith and inflicting emotional distress. A Los Angeles jury ordered tobacco giant Philip Morris to pay Betty Bullock $28 billion in punitive damages.

The Bullock award of $28 billion (which was lowered to $28 million and is still being appealed by Philip Morris) is by itself almost five times the combined amount of the top ten largest jury awards to individuals and families in 2001. Though a Department of Justice study showed that only a small percentage of cases are awarded punitive damages, and that the majority of awards are under $40,000, the number and amounts of punitive awards have been geometrically increasing since the high of $10,000 in 1959.

Some people argue that a fine is the best way to punish a corporation for acting wrongly. For example, the 1994 case against McDonald’s that won an elderly woman $2.7 million for spilling hot coffee in her lap is commonly seen as the beginning of our frivolous lawsuit period. What the jury heard, but most people did not, was that McDonald’s purposely kept its coffee at least forty degrees hotter than most restaurants did, as a cost-saving measure to extract more coffee from the beans; that more than 700 people had filed complaints of scalding coffee burns over the previous decade; and that McDonald’s knew their coffee was dangerously hot, yet had no plans to turn the heat down or postwarning signs. The woman in the case suffered third-degree burns to her groin, thighs, and buttocks that required skin grafts and a lengthy hospital stay. She filed suit against McDonald’s only after the company refused to pay her medical bills. Even the famous multimillion-dollar award was reduced on appeal to $480,000.

The true problem, many say, is not the size of such awards but the method by which we determine them. Punitive damages are not truly “damages” in the sense of compensation for a loss or injury but rather a fine, levied as punishment. In determining the amount of a punitive award, a jury is instructed to consider whether the defendant displayed reckless conduct, gross negligence, malice, or fraud—but in practice, a jury award often depends on how heart-tugging the plaintiff seems to be versus how heartless the big bad corporation appears.

Questions for Discussion

- Were the facts behind the McDonald’s lawsuit news to you? Do they change your opinion about this landmark case? What would you have done if you had been on the jury?

- Betty Bullock, who has lung cancer, had been a regular smoker for forty years and blamed Philip Morris for failing to warn her about smoking risks. Do you think Philip Morris is responsible? Do you think learning more about the case might change your opinion?

- Exxon was ordered to pay $125 million in criminal fines for the Exxon Valdez oil spill. In a separate trial, a civil jury hit Exxon with a $5 billion punitive award. Is it fair for a company to pay twice for the same crime?

- Are juries—composed of people who have no legal training, who know only about the case they are sitting on, who may be easily swayed by theatrical attorneys, and who are given only vague instructions—equipped to set punitive damage awards? Should punitive awards be regulated?

Sources: Kris Hudson, “Wal-Mart Workers Awarded $172 Million,” Wall Street Journal, December 23, 2005, B3; Olson, speech at the Manhattan Institute conference, “Crime and Punishment in Business Law,” May 8, 2002, reprinted at http://www.manhattan-institute.org/html/cjm_15.htm; “Surprise: Judges Hand Out Most Punitive Awards,” Wall Street Journal, June 12, 2000, 2b; Steven Brostoff, “Top Court to Review Punitive Damages,” National Underwriter Online News Service, June 27, 2002; “McFacts about the McDonalds Coffee Lawsuit,” Legal News and Views, Ohio Academy of Trial Lawyers, http://lawandhelp.com/q298–2.htm, Michael Bradford, “Phillip Morris to Continue Appeal of Punitives Award,” Business Insurance, December 19, 2002; http://www.altria.com/media/03_06_04_03_00_Bullock.asp for update on the Bullock case.

Exclusions and Exceptions

Whether the policy is open-perils or named-perils, the coverage it provides cannot be ascertained without considering the exclusionsPerils, risks, losses, and properties that are not covered in an all-risk policy., which are those perils, risks, losses, and properties that are not covered in an all-risk policy. Exclusions represent the third major part of an insurance policy and explicitly identify losses not covered by the policy. Usually, an insured may not know what the policy covers until he or she finds out what it does not cover. Unfortunately, this is not always an easy task. In many policies, exclusions appear not only under the heading “Exclusions” in one or more places but also throughout the policy and in various forms. When we delve into homeowners policies in Chapter 1 "The Nature of Risk: Losses and Opportunities", you will be amazed at the many exclusions, and exclusions to exclusions, that you will encounter. The homeowners policy section I (which provides property coverage) has two lists of exclusions identified as such, plus others scattered throughout the policy. The last sentence in the description of loss of use coverage, for example, says, “We do not cover loss or expense due to cancellation of a lease or agreement.” In other words, such loss is excluded. In “Perils Insured Against,” the policy at one point says, “We insure for risks of physical loss to the property…. Except,” followed by a list of losses or loss causes. Under the heading “Additional Coverages,” several types of coverage are listed and then the following sentence appears: “We do not cover loss arising out of business pursuits….” Thus, such loss is excluded.

A policy may exclude specified locations, perils, property, or losses. Perhaps a discussion of the exclusions in some policies and the reasons for them will be helpful.

Reasons for Exclusions

Let us review the reasons for the existence of exclusions. As noted in Chapter 6 "The Insurance Solution and Institutions", one reason exclusions exist is to avoid financial catastrophe for the insurer, which may result if many dependent exposures are insured or if a single, large-value exposure is insured. Because war would affect many exposures simultaneously, losses caused by war are excluded in most policies in order to avoid insuring catastrophic events. Exclusions also exist to limit coverage of nonfortuitous (that is, not accidental) events. Losses that are not accidental make prediction difficult, cause coverage to be expensive, and represent circumstances in which coverage would be contrary to public policy. As a result, losses caused intentionally (by the insured) are excluded. So, too, are naturally occurring losses that are expected. Wear and tear, for instance, is excluded from coverage. Adverse selection and moral hazard are limited by these exclusions.

Adverse selection is limited further by use of specialized policies and endorsements that standardize the risk. That is, limitations (exclusions) are placed in standard policies for exposures that are nonstandard. Those insureds who need coverage for such nonstandard exposures purchase it specifically. For example, homeowner’s policies limit theft coverage on jewelry and furs to a maximum amount ($2,500). Exposures in excess of the maximum are atypical, representing a higher probability (and severity) of loss than exists for the average homeowner. Insureds who own jewelry and furs with values in excess of the maximum must buy special coverage (if desired).

An important element is the point emphasized in the Links section at the beginning of the chapter. Some exclusions exist to avoid duplication of coverage by policies specifically intended to insure the exposure. As noted above, homeowners liability coverage excludes automobile liability, workers’ compensation liability, and other such exposures that are nonstandard to home and personal activities. Other policies specifically designed to cover such exposures are available and commonly used. To duplicate coverage would diminish insurers’ ability to discriminate among insureds and could result in moral hazard if insureds were paid twice for the same loss. A policy clause, termed other insurance clauseProvision in a policy that apportions the insurer’s financial responsibility so that payment in excess of the insured’s loss is avoided. (discussed in Chapter 9 "Fundamental Doctrines Affecting Insurance Contracts"), addresses the potential problem of duplicating coverage when two or more similar policies cover the same exposure. Through this type of provision, the insurer’s financial responsibility is apportioned so that payment in excess of the insured’s loss is avoided.

These reasons for exclusions are manifested in limitations on the following:

- Locations

- Perils

- Property

- Losses

The following is a discussion of the purposes of limiting locations, perils, property, and losses.

Excluded Locations

Some types of coverage are location-specific, such as to buildings. Other policies define the location of coverage. Automobile policies, for example, cover the United States and Canada. Mexico is not covered because of the very high auto risk there. In addition, some governmental entities in Mexico will not accept foreign insurance. Some property policies were written to cover movable property anywhere in the world except the Eastern bloc countries, likely because of difficulty in adjusting claims. With the breakup of the Communist bloc, these limitations are also being abandoned. Yet coverage may still be excluded where adjusting is difficult and/or the government of the location has rules against such foreign insurance. For a discussion of political risk—unanticipated political events that disrupt the earning or profit-making ability of an enterprise—see Chapter 11 "Property Risk Management".

Excluded Perils

Some perils are excluded because they can be covered by other policies or because they are unusual or catastrophic. The earthquake peril, for example, requires separate rating and is excluded from homeowners policies. This peril can be insured under a separate policy or added by endorsement for an extra premium. Many insureds do not want to pay the premium required, either because they think their property is not exposed to the risk of loss caused by an earthquake or because they expect that federal disaster relief would cover losses. Given the choice of a homeowners policy that excluded the earthquake peril and one that included earthquake coverage but cost $50 more per year, they would choose the former. Thus, to keep the price of their homeowners policies competitive, insurers exclude the earthquake peril. It is excluded also because it is an extraordinary peril that cannot easily be included with the other perils covered by the policy. It must be rated separately.

As noted above, perils, such as those associated with war, are excluded because commercial insurers consider them uninsurable. Nuclear energy perils, such as radiation, are excluded from most policies because of the catastrophic exposure. Losses to homeowners caused by the nuclear meltdown at Three Mile Island in 1979, which forced homeowners to evacuate the damaged property in the area, were not covered by their homeowners insurance. Losses due to floods are excluded and were a topic of much discussion after hurricanes Katrina and Rita. Losses due to wear and tear are excluded because they are inevitable rather than accidental and thus not insurable. Similarly, inherent vice, which refers to losses caused by characteristics of the insured property, is excluded. For example, certain products, such as tires and various kinds of raw materials, deteriorate with time. Such losses are not accidental and are, therefore, uninsurable.

Excluded Property

Some property is excluded because it is insurable under other policies. Homeowners policies, as previously stated, exclude automobiles because they are better insured under automobile policies. Other property is excluded because the coverage is not needed by the average insured, who would, therefore, not want to pay for it.

Liability policies usually exclude damage to or loss of others’ property in the care, custody, or control of the insured because property insurance can provide protection for the owner against losses caused by fire or other perils. Other possible losses, such as damage to clothing being dry cleaned, are viewed as a business risk involving the skill of the dry cleaner. Insurers do not want to assume the risk of losses caused by poor workmanship or poor management.

Excluded Losses

Losses resulting from ordinance or law—such as those regulating construction or repair—are excluded from most property insurance contracts. Policies that cover only direct physical damage exclude loss of use or income resulting from such damage. Likewise, policies covering only loss of use exclude direct losses. Health insurance policies often exclude losses (expenses) considered by the insurer to be unnecessary, such as the added cost of a private room or the cost of elective surgery.

Conditions

The fourth major part of an insurance contract is the conditions section. ConditionsClauses in a policy that enumerate the duties of the parties to the contract and, in some cases, define the terms used. enumerate the duties of the parties to the contract and, in some cases, define the terms used. Some policies list them under the heading “Conditions,” while others do not identify them as such. Wherever the conditions are stated, you must be aware of them. You cannot expect the insurer to fulfill its part of the contract unless you fulfill the conditions. Remember that acceptance of these conditions is part of the consideration given by the insured at the inception of an insurance contract. Failure to accept conditions may release the insurer from its obligations. Many conditions found in insurance contracts are common to all. Others are characteristic of only certain types of contracts. Some examples follow.

Notice and Proof of Loss

All policies require that the insurer be notified when the event, accident, or loss insured against occurs. The time within which notice must be filed and the manner of making it vary. The homeowners policy, for example, lists as one of the insured’s duties after loss to “give immediate notice to us or our agent” and to file proof of loss within sixty days. A typical life insurance policy says that payment will be made “upon receipt…of proof of death of the insured.” A health policy requires that “written proof of loss must be furnished to the Company within twelve months of the date the expense was incurred.” The personal auto policy says, “We must be notified promptly of how, when, and where the accident or loss happened.”

In some cases, if notice is not made within a reasonable time after the loss or accident, the insurer is relieved of all liability under the contract. A beneficiary who filed for benefits under an accidental death policy more than two years after the insured’s death was held in one case to have violated the notice requirement of the policy.Thomas v. Transamerica Occidental Life Ins. Co., 761 F. Supp. 709 (1991). The insurer is entitled to such timely notice so it can investigate the facts of the case. Insureds who fail to fulfill this condition may find themselves without protection when they need it most—after a loss.

Suspension of Coverage

Because there are some risks or hazardous situations insurers want to avoid, many policies specify acts, conditions, or circumstances that will cause the suspension of coverageRelease of the insurer from liability. or, in other words, that will release the insurer from liability. The effect is the same as if the policy were canceled or voided, but when a policy is suspended, the effect is only temporary. When a voidance of coverageTermination of coverage under an insurance policy. is incurred in an insurance contract, coverage is terminated. Protection resumes only by agreement of the insured and insurer. Suspension, in contrast, negates coverage as long as some condition exists. Once the condition is eliminated, protection immediately reverts without the need for a new agreement between the parties.

Some life and health policies have special clauses that suspend coverage for those in military service during wartime. When the war is over or the insured is no longer in military service, the suspension is terminated and coverage is restored. The personal auto policy has an exclusion that is essentially a suspension of coverage for damage to your auto. It provides that the insurer will not pay for loss to your covered auto “while it is used to carry persons or property for a fee,” except for use in a share-the-expense car pool. The homeowners policy (form 3) suspends coverage for vandalism and malicious mischief losses if the house has been vacant for more than thirty consecutive days. A property insurance policy may suspend coverage while there is “a substantial increase in hazard.”

You can easily overlook or misunderstand suspensions of coverage or releases from liability when you try to determine coverage provided by a policy. They may appear as either conditions or exclusions. Because their effect is much broader and less apparent than the exclusion of specified locations, perils, property, or losses, it is easy to underestimate their significance.

Cooperation of the Insured

All policies require your cooperation, in the sense that you must fulfill certain conditions before the insurer will pay for losses. Because the investigation of an accident and defense of a suit against the insured are very difficult unless he or she will cooperate, liability policies have a specific provision requiring cooperation after a loss. The businessowners policy, for example, says, “The insured shall cooperate with the Company, and upon the Company’s request, assist in…making of settlements; conducting of suits….”

It is not unusual for the insured to be somewhat sympathetic toward the claimant in a liability case, especially if the claimant is a friend. There have been situations in which the insured was so anxious for the claimant to get a large settlement from the insurer that the duty to cooperate was forgotten. If you do not meet this condition and the insurer can prove it, you may end up paying for the loss yourself. This is illustrated by the case of a mother who was a passenger in her son’s automobile when it was involved in an accident in which she was injured. He encouraged and aided her in bringing suit against him. The insurer was released from its obligations under the liability policy, on the grounds that the cooperation clause was breached.Beauregard v. Beauregard, 56 Ohio App. 158, 10 N.E.2d 227 (1937). The purpose of the cooperation clause is to force insureds to perform the way they would if they did not have insurance.

Protection of Property after Loss

Most property insurance policies contain provisions requiring the insured to protect the property after a loss in order to reduce the loss as much as possible. An insured who wrecks his or her automobile, for example, has the responsibility for having it towed to a garage for safekeeping. In the case of a fire loss, the insured is expected to protect undamaged property from the weather and other perils in order to reduce the loss. You cannot be careless and irresponsible just because you have insurance. Yet the requirement is only that the insured be reasonable. You are not required to put yourself in danger or to take extraordinary steps. Of course, views of what is extraordinary may differ.

Examination

A provision peculiar to some disability income policies gives the insurer the right to have its physician examine the insured periodically during the time he or she receives benefits under the policy. This right cannot be used to harass the claimant, but the insurer is entitled to check occasionally to see if he or she should continue to receive benefits. Property insurance policies have a provision that requires the claimant to submit to examination under oath, as well as make records and property available for examination by representatives of the insurance company.

Endorsements and Riders

Sometimes (maybe often), but not always, an insurance policy will include a fifth major part: the attachment of endorsements or riders. Riders and endorsements are two terms with the same meaning. Riders are used with life/health policies, whereas endorsements are used with property/casualty policies. A riderAttachment to a life/health insurance policy that changes the terms of the policy. makes a change in the life/health insurance policy to which it is attached; an endorsementAttachment to a the property/casualty insurance policy that changes the terms of the policy. makes a change in the property/casualty insurance policy to which it is attached. It may increase or decrease the coverage, change the premium, correct a statement, or make any number of other changes.

The endorsement guaranteeing home replacement cost, for example, provides replacement cost coverage for a dwelling insured by a homeowners policy, regardless of the limit of liability shown in the declarations. This keeps the amount of insurance on the dwelling up-to-date during the term of the policy. A waiver of premium rider increases the benefits of a life insurance policy by providing for continued coverage without continued payment of premiums if the insured becomes totally disabled. Endorsements and riders are not easier to read than the policies to which they are attached. Actually, the way some of them are glued or stapled to the policy may discourage you from looking at them. Nevertheless, they are an integral part of the contract you have with the insurer and cannot be ignored. When their wording conflicts with that in exclusions or other parts of the contract, the rider or endorsement takes precedence, negating the conflict.

Insurers continually add and change endorsements and riders to the policies as market conditions change and the needs are altered. For example, the commercial insurance units of Travelers Indemnity and Aetna Casualty and Surety provided an endorsement to protect contractors against third-party bodily injury and property damage claims arising out of accidental releases of pollutants they bring to job sites.“Travelers Construction Offers New Pollution Endorsements,” National Underwriter, Property & Casualty/Risk & Benefits Management Edition, March 10, 1997. Some features included were no time limits, full policy limits, and defense cost in addition to the basic full limits.

An example of a rider to life insurance policies is the estate tax repeal rider. This rider, which exemplifies the need to modify policies as tax laws change, was created in response to the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA 2001). Under this act, the federal estate tax will be phased out completely by 2010 but would return in 2011 unless Congress votes to eliminate it. If Congress eliminates the tax, the rider would let holders of the affected policies surrender the policies without paying surrender charges.“Hartford Introduces Estate-Tax Repeal Rider,” National Underwriter Online News Service, April 1, 2002; “Lincoln Life Expands Estate Tax Safety Net on Life Insurance” National Underwriter Online News Service, Oct. 12, 2001.

Another example of a rider relates to long-term care (LTC) insurance (discussed in Chapter 2 "Risk Measurement and Metrics"). Most long-term care policies include a rider offering some sort of inflation protection, generally 5 percent annually.Jack Crawford, “Inflation Protection: Is the LTC Industry on the Right Path?” National Underwriter, Life & Health/Financial Services Edition, January 21, 2002.

Key Takeaways

In this section you studied the five basic parts of insurance contracts:

- Declarations—specify periods of coverage, place limitations on liability, and stipulate the insured’s loss retention provisions

- Insuring agreement—statement of general promise made to the insured; determines whether policy covers named-perils or open-perils; provides exposures to be covered and types of losses

- Exclusions—state what losses/causes of loss the policy does not cover because of limitations on locations, perils, property, and losses

- Conditions—define the duties of the parties to the contract; notice and proof of loss mandates, suspension of coverage triggers, cooperation of the insured requirement, protection of property after loss measures, and physical examination right

- Endorsements and riders—optional elements that change the terms of property/casualty and life/health policies; take precedence when they conflict with other parts of the contract

Discussion Questions

- What are the main reasons for exclusions and for endorsements and riders in insurance policies?

- What is the significance of an open-perils policy? In deciding between a named-perils policy and an open-perils policy, what factors would you consider? Define both terms and explain your answer.

- In Chapter 1 "The Nature of Risk: Losses and Opportunities" on automobile insurance, you will find that portable stereos and tape decks are excluded from coverage. What do you think the insurance company’s rationale is for such an exclusion? What are other reasons for insurance policy exclusions? Give examples of each.

- Lightning struck a tree in the Gibsons’ yard, causing it to fall over and smash the bay window in their living room. The Gibsons were so distraught by the damage that they decided to go out for dinner to calm themselves. After dinner, the Gibsons decided to take in a movie. When they returned home, they discovered that someone had walked through their broken bay window and stolen many of their valuable possessions. The Gibsons have a homeowners policy that covers both physical damage and theft. As the Gibsons’ insurer, do you cover all their incurred losses? Why or why not?

- Your careless driving results in serious injury to Linda Helsing, a close personal friend. Because she knows you have liability insurance and the insurer will pay for damages on your behalf, she files suit against you. Would it be unreasonable for your insurer to expect you not to help Linda pursue maximum recovery in every conceivable way? Explain.

10.3 Review and Practice

- Describe a few exclusions and a few endorsements and riders.

- Joe Phelps is a chemistry aficionado. For his twenty-ninth birthday last month, Joe’s wife bought him an elaborate chemistry set to use in their attached garage. The set includes dangerous (flammable) substances, yet Joe does not notify his homeowner’s insurer. What problem might Joe encounter?

- Joe has another insurance problem. He had an automobile accident last month in which he negligently hit another motorist while turning right on red. The damage was minor, so Joe just paid the other motorist for the repairs. Fearing the increase in his auto insurance premiums, Joe did not notify his insurer of the accident. Now the other motorist is suing for whiplash. What is Joe’s problem, and why?

-

“A Federal Reserve Board survey showing that banks are still making commercial real estate loans for ‘high profile’ properties does not tell the whole story of the impact of problems in the terrorism insurance market, insurance industry officials contend” (Steven Brostoff, “Loans Still Coming Despite Terror Risks,” National Underwriter, Property & Casualty/Risk & Benefits Management Edition, June 3, 2002).

- Relate this story to the terrorism exclusion information you found in this chapter.

- What is the actual problem?

- “States approving terrorism exclusions for commercial property insurance are a help to the insurance industry, but two critical exposures aren’t excluded from terrorism—workers’ compensation and fire following a terrorist event” (“Even with Exclusions, Insurers Still Exposed to Workers’ Comp, Fire Losses,” Best’s Insurance News, January 10, 2002.) What can be the impact on insurers’ bottom line when such exclusions are not adopted?

-

Kevin Kaiser just replaced his old car with a new one and is ready to drive the new car off the lot. He did not have collision insurance on the old car, but he wants some on the new one. He calls his friend Dana Goldman, who is an insurance agent. “Give me the works, Dana. I want the best collision coverage you have.” Soon after he drives the car away from the lot, he is struck by an eighteen-wheeler and the new car is totaled.

Kevin then discovers that he has collision insurance with a $500 deductible, which he must pay. He is upset because to him “the works” meant full insurance for all losses he might have due to collision. Dana had thought that he wanted more cost-efficient coverage and had used the deductible to lower the premium. The applicable state law and insurer underwriting practices allow deductibles as low as $250, although they can be much higher.

- Kevin wants to take Dana to court to collect the full value of the auto. What would you advise him?

- What does this tell you about oral contracts?

- What are the shortcomings of limited-peril health insurance policies, such as coverage for loss caused solely by cancer, from a personal risk management point of view?

-

A. J. Jackson was very pleased to hear the agent say that she was covered the moment she finished completing the application and paid the agent the first month’s premium for health insurance. A. J. had had some health problems previously and really didn’t expect to be covered until after she had taken her physical and received notice from the company. The agent said that the conditional binder was critical for immediate coverage. “Of course,” said the agent, “this coverage may be limited until the company either accepts or rejects your application.” The agent congratulated A. J. again for her decision. A. J. began to wonder the next morning exactly what kind of coverage, if any, she had.

- What kind of coverage did A. J. have?

- Did her submission to the agent of the first month’s premium have any impact on her coverage? Why?

- If you were the agent, how would you have explained this coverage to A. J.?

-

LeRoy Leetch had a heck of a year. He suffered all the following losses. Based on what you know about insurance, which would you expect to be insurable and why?

- LeRoy’s beloved puppy, Winchester, was killed when struck by a school bus. He has losses of burial expenses, the price of another puppy, and his grief due to Winchester’s death.

- LeRoy has an expensive collection of rare clocks. Most are kept in his spare bedroom and were damaged when a fire ignited due to faulty wiring. The loss is valued at $15,000.

- Heavy snowfall and a rapid thaw caused flooding in LeRoy’s town. Damage to his basement was valued at $2,200.

- Weather was hard on the exterior of LeRoy’s house as well. Dry rot led to major damage to the first-story hardwood floors. Replacement will cost $6,500.

- When you apply for a life insurance policy, agent Dawn Gale says, “If you will give me your check for the first month’s premium now, the policy will cover you now if you are insurable.” Is this a correct statement, or is Dawn just in a hurry to get her commission for selling you the policy? Explain.