This is “Operating Leases versus Capital Leases”, section 15.2 from the book Business Accounting (v. 2.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

15.2 Operating Leases versus Capital Leases

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Account for an operating lease, realizing that the only liability to be reported is the amount that is currently due.

- Understand that the only asset reported in connection with an operating lease is prepaid rent if payments are made in advance.

- Record the initial entry for a capital lease with both the asset and the liability calculated at the present value of the future cash flows.

- Explain the interest rate to be used by the lessee in determining the present value of a capital lease and the amount of interest expense to be recognized each period.

- Determine and recognize the depreciation of an asset recorded as the result of a capital lease.

The Financial Reporting of an Operating Lease

Question: The Abilene Company has agreed to pay $100,000 per year for seven years to lease an airplane. Assume that legal title will not be received by Abilene and no purchase option is mentioned in the contract. Assume also that the life of the airplane is judged to be ten years and the payments do not approximate the fair value of the item.

The contract is signed on December 31, Year One, with the first annual payment made immediately. Based on the description of the agreement, none of the four criteria for a capital lease have been met. Thus, Abilene has an operating lease. What financial accounting is appropriate for an operating lease?

Answer: None of the four criteria for a capital lease is met in this transaction:

- Legal ownership is not conveyed to the lessee.

- No bargain purchase option is included in the contract.

- The life of the lease is less than 75 percent of the life of asset (seven years out of ten years or 70 percent).

- Payments do not approximate the acquisition value of the asset.

Thus, Abilene is just renting the airplane and agrees on an operating lease. The first annual payment was made immediately to cover the subsequent year.

Figure 15.1 December 31, Year One—Payment of First Installment of Operating Lease

Because the first payment has been made, no liability is reported on Abilene’s balance sheet although the contract specifies that an additional $600,000 in payments will be required over the subsequent six years. In addition, the airplane itself is not shown as an asset by the lessee. The operating lease is viewed as the equivalent of a rent and not a purchase.

During Year Two, as time passes, the future value provided by the first prepayment gradually becomes a past value. The asset balance is reclassified as an expense. At the end of that period, the second payment will also be made.

Figure 15.2 December 31, Year Two—Adjustment to Record Rent Expense for Year Two

Figure 15.3 December 31, Year Two—Payment of Second Installment of Operating Lease

Initial Recording of a Capital Lease

Question: One slight change can move this contract from an operating lease to a capital lease. Assume all the information remains the same in the previous example except that the airplane has an expected life of only nine years rather than ten. With that minor alteration, the life of the lease is 77.8 percent of the life of the asset (seven years out of nine years). The contract is now 75 percent or more of the life of the asset. Because one of the criteria is now met, this contract must be viewed as a capital lease. The change in that one estimation creates a major impact on the reporting process. How is a capital lease reported initially by the lessee?

Answer: As a capital lease, the transaction is reported in the same manner as a purchase. Abilene has agreed to pay $100,000 per year for seven years, but no part of this amount is specifically identified as interest. According to U.S. GAAP, if a reasonable rate of interest is not explicitly paid each period, a present value computation is required to split the contractual payments between principal (the amount paid for the airplane) and interest (the amount paid to extend payment over this seven-year period). This accounting is not only appropriate for an actual purchase when payments are made over time but also for a capital lease.

Before the lessee computes the present value of the future cash flows, one issue must be resolved. A determination is needed of the appropriate rate of interest to be applied. In the previous discussion of bonds, a negotiated rate was established between the investor and the issuing company. No such bargained rate exists in connection with a lease. According to U.S. GAAP, the lessee should use its own incremental borrowing rate. That is the interest rate the lessee would be forced to pay to borrow this same amount of money from a bank or other lending institution.As explained in upper-level accounting textbooks, under certain circumstances, the lessee might use the implicit interest rate built into the lease contract by the lessor. Assume here that the incremental borrowing rate for Abilene is 10 percent per year. If the company had signed a loan to buy this airplane instead of lease it, the assumption is that the lender would have demanded an annual interest rate of 10 percent.

Abilene will pay $100,000 annually over these seven years. Because the first payment is made immediately, these payments form an annuity due. As always, the present value calculation computes the interest at the appropriate rate and then removes it to leave the principal: the amount of the debt incurred to obtain the airplane. Once again, present value can be found by table (in the following link or included at the end of this book), by formula, or by Excel spreadsheet.On an Excel spreadsheet, the present value of a $1 per period annuity due for seven periods at an assumed annual interest rate of 10 percent is computed by typing the following data into a cell: =PV(.10,7,1,,1).

Present Value of an Annuity Due of $1

http://www.principlesofaccounting.com/ART/fv.pv.tables/pvforannuitydue.htm

Present value of an annuity due of $1 per year for seven years at a 10 percent annual interest rate is $5.35526. The present value of seven payments of $100,000 is $535,526.

present value = $100,000 × 5.35526 present value = $535,526After the present value has been determined, the recording of the capital lease proceeds very much like a purchase made by signing a long-term liability.

Figure 15.4 December 31, Year One—Capital Lease Recorded at Present Value

Figure 15.5 December 31, Year One—Initial Payment on Capital Lease

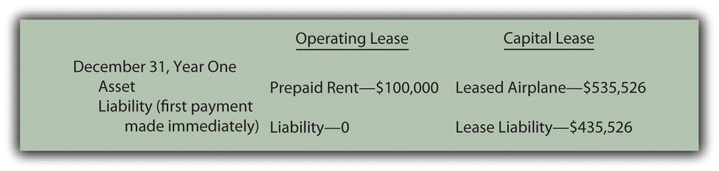

A comparison at this point between the reporting of an operating lease and a capital lease is striking. The differences are not inconsequential. For the lessee, good reasons exist for seeking an operating lease rather than a capital lease.

Figure 15.6 Comparison of Initially Reported Amounts for an Operating Lease and for a Capital Lease

Test Yourself

Question:

A company signs a lease on January 1, Year One, to lease a machine for eight years. Payments are $10,000 per year with the first payment made immediately. The company has an incremental borrowing rate of 6 percent. This lease qualifies as a capital lease. The present value of an ordinary annuity of $1 for eight periods at an annual interest rate of 6 percent is $6.20979. The present value of an annuity due of $1 for eight periods at an annual interest rate of 6 percent is $6.58238. If financial statements are produced after this lease has been signed and settled, which of the following balances will be reported (rounded)?

- Leased asset of $62,098 and lease liability of $52,098

- Leased asset of $52,098 and lease liability of $62,098

- Leased asset of $65,824 and lease liability of $55,824

- Leased asset of $55,824 and lease liability of $65,824

Answer:

The correct answer is choice c: Leased asset of $65,824 and lease liability of $55,824.

Explanation:

Because the first payment is made immediately, this contract is classified as an annuity due. As a capital lease, both the asset and the liability are initially reported at the present value of these cash flows at the lessee’s incremental borrowing rate or $65,824 ($10,000 × $6.5824). However, the first $10,000 payment is also made at that time so the liability balance is reduced by that amount.

Accounting for a Capital Lease over Time

Question: In a capital lease, property is not bought but is accounted for as if it had been purchased. When the contract is signed in the previous example, Abilene records both the leased airplane and the liability at the present value of the required cash payments. What reporting takes place subsequent to the initial recording of a capital lease transaction?

Answer: As with any purchase of an asset having a finite life where payments extend into the future, the cost of the asset is depreciated, and interest is recognized in connection with the liability. This process remains the same whether the asset is bought or obtained by capital lease.

Depreciation. The airplane will be used by Abilene for the seven-year life of the lease. The recorded cost of the asset is depreciated over this period to match the expense recognition with the revenue that the airplane helps generate. Assuming the straight-line method is applied, annual depreciation is $76,504 (rounded) or $535,526/seven years.

Interest. The principal of the lease liability during Year Two is $435,526. That balance is the initial $535,526 present value less the first payment of $100,000. The annual interest rate used in determining present value was 10 percent so interest expense of $43,553 (rounded) is recognized for this period of time—the liability principal of $435,526 times this 10 percent annual rate. As in the chapter on bonds and notes, the effective rate method is applied here.

Figure 15.7 December 31, Year Two—Depreciation of Airplane Obtained in Capital Lease

Figure 15.8 December 31, Year Two—Interest on Lease Liability from Capital Lease

Figure 15.9 December 31, Year Two—Second Payment on Capital Lease

Test Yourself

Question:

A company leases a truck for its operations. The accountant is attempting to determine if this lease is a capital lease or an operating lease. Which of the following statements is true?

- The reported liability balance is likely to be higher in an operating lease.

- A prepaid rental account is likely to be reported in a capital lease.

- The leased asset will appear in the financial statements if this is an operating lease.

- Both depreciation expense and interest expense are recognized for a capital lease.

Answer:

The correct answer is choice d: Both depreciation expense and interest expense are recognized for a capital lease.

Explanation:

In an operating lease, a prepaid rent account is established by the cash payments with that amount then reclassified to rent expense as time passes. Little or no liability is reported. In a capital lease, both the asset and the liability are reported at the present value of the future cash payments. The cost attributed to the asset is depreciated while interest expense must be recognized on the liability balance each period.

Talking with an Independent Auditor about International Financial Reporting Standards

Following is a continuation of our interview with Robert A. Vallejo, partner with the accounting firm PricewaterhouseCoopers.

Question: In U.S. GAAP, if a lease arrangement meets any one of four criteria, the transaction is reported as a capital lease. Companies often design transactions to either avoid or meet these criteria based on the desired method of accounting. Do IFRS requirements utilize the same set of criteria to determine whether a capital lease or an operating lease has been created?

Rob Vallejo: This is difficult to answer based on the current status of the FASB and IASB’s joint project on “Leases” that began with a discussion paper in 2009. After receiving a large number of comments on a draft version of a new standard, the FASB and IASB are currently making revisions and will release a new draft version in the first half of 2012. Regardless of the outcome, after the new standard is issued (effective date could be as early as 2014), the distinction between operating and capital leases will be eliminated, as all leases will be treated as finance leases and included on the balance sheet at inception. For organizations that have structured leases to meet the definition of an operating lease, the new standard will have a significant impact. Officials should already be considering the implications to their financial statements and ongoing financial reporting. To check the latest status of the FASB and IASB’s joint project on leases, check the FASB’s web-site, http://www.FASB.org. Currently, a leasing arrangement may well be classified differently under IFRS than under U.S. GAAP. This is an example of where existing U.S. GAAP has rules and IFRS has principles. Under today’s U.S. GAAP, guidance is very specific based on the four rigid criteria established by FASB. However, under IFRS, the guidance focuses on the substance of the transaction and there are no quantitative breakpoints or bright lines to apply. For example, there is no definitive rule such as the “75 percent of the asset’s life” criterion found in U.S. GAAP. IFRS simply asks the question: have all the risks and rewards of ownership been substantially transferred?

Key Takeaway

Operating leases record payment amounts as they come due and are paid. Therefore, the only reported asset is a prepaid rent, and the liability is the current amount due. For a capital lease, the present value of all future cash payments is determined using the incremental borrowing rate of the lessee. The resulting amount is recorded as both the leased asset and the lease liability. The asset is then depreciated over the time that the lessee will make use of it. Interest expense is recorded (along with periodic payments) in connection with the liability as time passes using the effective rate method.