This is “Target Markets and Modes of Entry”, chapter 5 from the book Global Strategy (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

Chapter 5 Target Markets and Modes of Entry

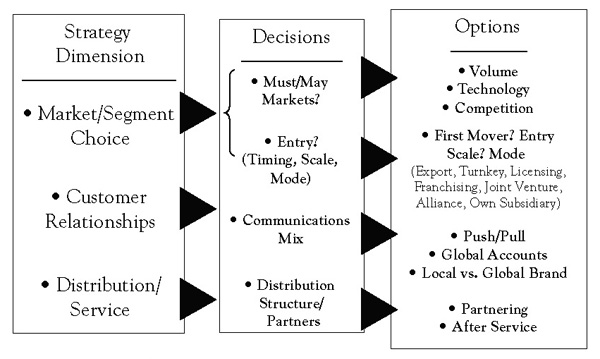

Market participation decisions—selecting global target markets, entry modes, and how to communicate with customers all over the world—are intimately related to decisions about how much to adapt the company’s basic value proposition. The choice of customers to serve in a particular country or region and with a particular culture determines how and how much a company must adapt its basic value proposition. Conversely, the extent of a company’s capabilities to tailor its offerings around the globe limits or broadens its options to successfully enter new markets or cultures. In this chapter, we look at the first two of these decisions: selecting target markets around the world and deciding how best to enter them. In Chapter 6 "Globalizing the Value Proposition", we introduce a framework for analyzing choices about adapting a company’s basic value proposition. In Chapter 7 "Global Branding", we take up global branding, one of a company’s primary vehicles for communicating with customers all over the world (Figure 5.1 "Market Participation").

5.1 Target Market Selection

Few companies can afford to enter all markets open to them. Even the world’s largest companies such as General Electric or Nestlé must exercise strategic discipline in choosing the markets they serve. They must also decide when to enter them and weigh the relative advantages of a direct or indirect presence in different regions of the world. Small and midsized companies are often constrained to an indirect presence; for them, the key to gaining a global competitive advantage is often creating a worldwide resource network through alliances with suppliers, customers, and, sometimes, competitors. What is a good strategy for one company, however, might have little chance of succeeding for another.

Figure 5.1 Market Participation

The track record shows that picking the most attractive foreign markets, determining the best time to enter them, and selecting the right partners and level of investment has proven difficult for many companies, especially when it involves large emerging markets such as China. For example, it is now generally recognized that Western carmakers entered China far too early and overinvested, believing a “first-mover advantage” would produce superior returns. Reality was very different. Most companies lost large amounts of money, had trouble working with local partners, and saw their technological advantage erode due to “leakage.” None achieved the sales volume needed to justify their investment.

Even highly successful global companies often first sustain substantial losses on their overseas ventures, and occasionally have to trim back their foreign operations or even abandon entire countries or regions in the face of ill-timed strategic moves or fast-changing competitive circumstances. Not all of Wal-Mart’s global moves have been successful, for example—a continuing source of frustration to investors. In 1999, the company spent $10.8 billion to buy British grocery chain Asda. Not only was Asda healthy and profitable, but it was already positioned as “Wal-Mart lite.” Today, Asda is lagging well behind its number-one rival, Tesco. Even though Wal-Mart’s UK operations are profitable, sales growth has been down in recent years, and Asda has missed profit targets for several quarters running and is in danger of slipping further in the UK market.

This result comes on top of Wal-Mart’s costly exit from the German market. In 2005, it sold its 85 stores there to rival Metro at a loss of $1 billion. Eight years after buying into the highly competitive German market, Wal-Mart executives, accustomed to using Wal-Mart’s massive market muscle to squeeze suppliers, admitted they had been unable to attain the economies of scale it needed in Germany to beat rivals’ prices, prompting an early and expensive exit.

What makes global market selection and entry so difficult? Research shows there is a pervasive the-grass-is-always-greener effect that infects global strategic decision making in many, especially globally inexperienced, companies and causes them to overestimate the attractiveness of foreign markets.Ghemawat (2001). As noted in Chapter 1 "Competing in a Global World", “distance,” broadly defined, unless well-understood and compensated for, can be a major impediment to global success: cultural differences can lead companies to overestimate the appeal of their products or the strength of their brands; administrative differences can slow expansion plans, reduce the ability to attract the right talent, and increase the cost of doing business; geographic distance impacts the effectiveness of communication and coordination; and economic distance directly influences revenues and costs.

A related issue is that developing a global presence takes time and requires substantial resources. Ideally, the pace of international expansion is dictated by customer demand. Sometimes it is necessary, however, to expand ahead of direct opportunity in order to secure a long-term competitive advantage. But as many companies that entered China in anticipation of its membership in the World Trade Organization have learned, early commitment to even the most promising long-term market makes earning a satisfactory return on invested capital difficult. As a result, an increasing number of firms, particularly smaller and midsized ones, favor global expansion strategies that minimize direct investment. Strategic alliances have made vertical or horizontal integration less important to profitability and shareholder value in many industries. Alliances boost contribution to fixed cost while expanding a company’s global reach. At the same time, they can be powerful windows on technology and greatly expand opportunities to create the core competencies needed to effectively compete on a worldwide basis.

Finally, a complicating factor is that a global evaluation of market opportunities requires a multidimensional perspective. In many industries, we can distinguish between “must” marketsThose markets in which a firm must compete in order to realize its global ambitions.—markets in which a company must compete in order to realize its global ambitions—and “nice-to-be-in” marketsMarkets in which participation is desirable but not critical.—markets in which participation is desirable but not critical. “Must” markets include those that are critical from a volume perspective, markets that define technological leadership, and markets in which key competitive battles are played out. In the cell phone industry, for example, Motorola looks to Europe as a primary competitive battleground, but it derives much of its technology from Japan and sales volume from the United States.

5.2 Measuring Market Attractiveness

Four key factors in selecting global markets are (a) a market’s size and growth rate, (b) a particular country or region’s institutional contexts, (c) a region’s competitive environment, and (d) a market’s cultural, administrative, geographic, and economic distance from other markets the company serves.

Market Size and Growth Rate

There is no shortage of country information for making market portfolio decisions. A wealth of country-level economic and demographic data are available from a variety of sources including governments, multinational organizations such as the United Nations or the World Bank, and consulting firms specializing in economic intelligence or risk assessment. However, while valuable from an overall investment perspective, such data often reveal little about the prospects for selling products or services in foreign markets to local partners and end users or about the challenges associated with overcoming other elements of distance. Yet many companies still use this information as their primary guide to market assessment simply because country market statistics are readily available, whereas real product market information is often difficult and costly to obtain.

What is more, a country or regional approach to market selection may not always be the best. Even though Theodore Levitt’s vision of a global market for uniform products and services has not come to pass, and global strategies exclusively focused on the “economics of simplicity” and the selling of standardized products all over the world rarely pay off, research increasingly supports an alternative “global segmentation” approach to the issue of market selection, especially for branded products. In particular, surveys show that a growing number of consumers, especially in emerging markets, base their consumption decisions on attributes beyond direct product benefits, such as their perception of the global brands behind the offerings.

Specifically, research by John Quelch and others suggests that consumers increasingly evaluate global brands in “cultural” terms and factor three global brand attributes into their purchase decisions: (a) what a global brand signals about quality, (b) what a brand symbolizes in terms of cultural ideals, and (c) what a brand signals about a company’s commitment to corporate social responsibility. This creates opportunities for global companies with the right values and the savvy to exploit them to define and develop target markets across geographical boundaries and create strategies for “global segmentsComprised of consumers who evaluate global brands in “cultural” terms and factor global brand attributes into their purchase decisions.” of consumers. Specifically, consumers who perceive global brands in the same way appear to fall into one of four groups:

- Global citizens rely on the global success of a company as a signal of quality and innovation. At the same time, they worry whether a company behaves responsibly on issues like consumer health, the environment, and worker rights.

- Global dreamers are less discerning about, but more ardent in their admiration of, transnational companies. They view global brands as quality products and readily buy into the myths they portray. They also are less concerned with companies’ social responsibilities than global citizens.

- Antiglobals are skeptical that global companies deliver higher-quality goods. They particularly dislike brands that preach American values and often do not trust global companies to behave responsibly. Given a choice, they prefer to avoid doing business with global firms.

- Global agnostics do not base purchase decisions on a brand’s global attributes. Instead, they judge a global product by the same criteria they use for local brands.Quelch (2003, August); Holt, Quelch, and Taylor (2004, September).

Companies that use a “global segment” approach to market selection, such as Coca-Cola, Sony, or Microsoft, to name a few, therefore must manage two dimensions for their brands. They must strive for superiority on basics like the brand’s price, performance, features, and imagery, and, at the same time, they must learn to manage brands’ global characteristics, which often separate winners from losers. A good example is provided by Samsung, the South Korean electronics maker. In the late 1990s, Samsung launched a global advertising campaign that showed the South Korean giant excelling, time after time, in engineering, design, and aesthetics. By doing so, Samsung convinced consumers that it successfully competed directly with technology leaders across the world, such as Nokia and Sony. As a result, Samsung was able to change the perception that it was a down-market brand, and it became known as a global provider of leading-edge technologies. This brand strategy, in turn, allowed Samsung to use a global segmentation approach to making market selection and entry decisions.

Institutional ContextsKhanna, Palepu, and Sinha (2005).

Khanna and others developed a five-dimensional framework to map a particular country or region’s institutional contextsComprised of a country or region’s political and social systems, openness, product markets, labor markets, and capital markets.. Specifically, they suggest careful analysis of a country’s (a) political and social systems, (b) openness, (c) product markets, (d) labor markets, and (e) capital markets.

A country’s political system affects its product, labor, and capital markets. In socialist societies like China, for instance, workers cannot form independent trade unions in the labor market, which affects wage levels. A country’s social environment is also important. In South Africa, for example, the government’s support for the transfer of assets to the historically disenfranchised native African community has affected the development of the capital market.

The more open a country’s economy, the more likely it is that global intermediaries can freely operate there, which helps multinationals function more effectively. From a strategic perspective, however, openness can be a double-edged sword: a government that allows local companies to access the global capital market neutralizes one of the key advantages of foreign companies.

Even though developing countries have opened up their markets and grown rapidly during the past decade, multinational companies struggle to get reliable information about consumers. Market research and advertising are often less sophisticated and, because there are no well-developed consumer courts and advocacy groups in these countries, people can feel they are at the mercy of big companies.

Recruiting local managers and other skilled workers in developing countries can be difficult. The quality of local credentials can be hard to verify, there are relatively few search firms and recruiting agencies, and the high-quality firms that do exist focus on top-level searches, so companies scramble to identify middle-level managers, engineers, or floor supervisors.

Capital and financial markets in developing countries often lack sophistication. Reliable intermediaries like credit-rating agencies, investment analysts, merchant bankers, or venture capital firms may not exist, and multinationals cannot count on raising debt or equity capital locally to finance their operations.

Emerging economies present unique challenges. Capital markets are often relatively inefficient and dependable sources of information, scarce while the cost of capital is high and venture capital is virtually nonexistent. Because of a lack of high-quality educational institutions, labor markets may lack well-trained people requiring companies to fill the void. Because of an underdeveloped communications infrastructure, building a brand name can be difficult just when good brands are highly valued because of lower product quality of the alternatives. Finally, nurturing strong relationships with government officials often is necessary to succeed. Even then, contracts may not be well enforced by the legal system.

Competitive Environment

The number, size, and quality of competitive firms in a particular target market compose a second set of factors that affect a company’s ability to successfully enter and compete profitably. While country-level economic and demographic data are widely available for most regions of the world, competitive data are much harder to come by, especially when the principal players are subsidiaries of multinational corporations. As a consequence, competitive analysis in foreign countries, especially in emerging markets, is difficult and costly to perform and its findings do not always provide the level of insight needed to make good decisions. Nevertheless, a comprehensive competitive analysis provides a useful framework for developing strategies for growth and for analyzing current and future primary competitors and their strengths and weaknesses.The competitive environment of a country or region is affected by the number, size, and quality of competitive firms already present in a particular target market.

Minicase: Which BRIC Countries? A Key Challenge for CarmakersHaddock and Jullens (2009).

Today, automobile manufacturers face a critical challenge: deciding which BRIC countries (Brazil, Russia, India, and China) to bet on. In each, as per capita income rises, so will per capita car ownership—not in a straight line but in classic “S-curve” fashion. Rates of vehicle ownership stay low during the first phases of economic growth, but as the GDP or purchasing power of a country reaches a level of sustained broad prosperity, and as urbanization reshapes the work patterns of a country, vehicle sales take off. But that is about where the similarities end. Each of the four BRIC nations has a completely different set of market and industry dynamics that make decision choices about which countries to target, including making difficult decisions about which markets to avoid, extremely difficult.

For one thing, vehicle manufacturing is a high-profile industry that generates enormous revenue, employs millions of people, and is often a proxy for a nation’s manufacturing prowess and economic influence. Governments are extensively involved in regulating or influencing virtually every aspect of the product and the way the industry operates—including setting emissions and safety standards, licensing distributors, and setting tariffs and rules about how much manufacturing must take place locally. This reality makes the job of understanding each market and appreciating the differences more vital. For example, a summary overview of the BRIC nations reveals the differences among these markets and the operating complexities in all of them.

Brazil, with Russia, is one of the smaller BRIC countries, with 188 million people (by comparison, China and India each have more than 1 billion, Russia has 142 million). Yet car usage is already relatively high: 104 cars in use per 1,000 people, nearly 10 times the rate of usage in India, according to the Economist Intelligence Unit. Because of this, growth projections for Brazil are relatively low—more in line with developed nations than with the other BRIC countries. Projections made by the industry research firm Global Insight show that sales will grow just 2% until 2013, underperforming even the U.S. market’s projected growth rate.

On the plus side, Brazil is socioeconomically stable, with increasing wealth and a maturing finance system that is helping to propel growth among rural, first-time buyers who prefer compact cars. Few domestic brands exist, as the market is dominated by GM, Ford, Fiat, and Volkswagen. Prompted by generous government incentives, high import taxes, and exchange rate risks, foreign automakers have invested significantly in Brazil, which has thus become an unrivaled production hub for the rest of South America. Brazilian consumers live in a country with large rural areas and very rough terrain; they demand fairly large, SUV-like cars, made with economical small engines and flex-fuel power trains friendly to the country’s biofuel industry. When a Latin American family buys its first automobile, chances are it was made in Brazil.

Russia, even though it is the smallest of the BRIC countries in population, has the highest auto adoption of the four: 213 cars in use per 1,000 people. (Western Europe, by comparison, has 518, according to the Economist Intelligence Unit.) Yet Global Insight expects future sales growth to average 6.5% from 2008 to 2013, far outpacing Brazil (2%), Western Europe (1.2%), and Japan and Korea (0.2%).

Given Russia’s proximity to Europe, consumer preferences there are more akin to those of the developed markets than to those of China or India, and expensive, status-enhancing European models remain popular, although European safety features, interior components, and electronics are often stripped out to reduce costs. For vehicle manufacturers, the attractions of the Russian market include an absence of both local partnership requirements and significant local competitors. But there is high political risk. So far, the Russian government has permitted foreign carmakers to operate relatively freely, but the Kremlin’s history of meddling in private enterprise and undercutting private ownership worries some executives. These concerns were heightened in November 2008, when Russia implemented tariffs against car imports in hopes of avoiding layoffs that might spark labor unrest among the country’s 1.5 million car industry workers.

India has 1.1 billion people, but its level of car adoption is still low, with only 11 cars in use per 1,000 people. The upside is higher potential growth: among the BRIC countries, India is expected to have the fastest-growing auto sales, almost 15% per year until 2013, according to Global Insight. Sales of subcompact cars are strong, even during the global recession. The popularity of these small cars combines with India’s energy shortages and the country’s chronic pollution to provide foreign carmakers with an ideal opportunity to further develop electric power-train technologies there.

Until the early 1990s, foreign automobile manufacturers were mostly shut out of India. That has changed radically. Today, foreign automakers are welcomed and the government promotes foreign ownership and local manufacturing with tax breaks and strong intellectual property protection. And because foreign companies were shut out for a long period of time, India has capable manufacturers and suppliers for foreign vehicle manufacturers to partner with. Local competition is strong but is thus far concentrated among three players: Maruti Suzuki India, Ltd., Tata, and the Hyundai Corporation, which is well established in India.

China is almost as large as the other three combined in total auto sales and production. Its overall auto usage is just 18 cars per 1,000 households, but annual sales growth until 2013 is expected to be almost 10%. Its size and growth potential make China a dominant force in the industry going forward; new models and technologies developed there will almost certainly become available elsewhere.

But the Chinese government plays a central role in shaping the auto industry. Current ownership policies mandate that foreign vehicle manufacturers enter into 50-50 joint ventures with local automakers, and poor intellectual property rights enforcement puts the design and engineering innovations of foreign car companies at constant risk. At the same time, to cope with energy shortages and rampant pollution, the Chinese government is strongly encouraging research and development on alternative power trains, including electric cars and gasoline-electric hybrids. As a result, Chinese car companies may develop significant power-train capabilities ahead of their competitors.

Like their Indian counterparts, Chinese car companies have outpaced global automakers in developing cars specifically for emerging markets. A few Western companies, like Volkswagen AG, which has sold its Santana models in China through a joint venture (Shanghai Volkswagen Automotive Company) since 1985, are competitive. Some Chinese carmakers, like BYD Company, aspire to become global leaders in the industry. But many suffer from a talent shortage and inexperience in managing across borders. This may prompt them to acquire all or part of distressed Western automobile companies in the near future or to hire skilled auto executives from established companies and their suppliers.

In short, each of the four BRIC nations has a completely different set of market and industry dynamics. And the same is true for the other developing nations. Meanwhile, the number of autos in use in the developing world is projected to expand almost six-fold by 2018.

Cultural, Administrative, Geographic, and Economic Distance

Explicitly considering the four dimensions of distance introduced in Chapter 1 "Competing in a Global World" can dramatically change a company’s assessment of the relative attractiveness of foreign markets. In his book The Mirage of Global Markets, David Arnold describes the experience of Mary Kay Cosmetics (MKC) in entering Asian markets. MKC is a direct marketing company that distributes its products through independent “beauty consultants” who buy and resell cosmetics and toiletries to contacts either individually or at social gatherings. When considering market expansion in Asia, the company had to choose: enter Japan or China first? Country-level data showed Japan to be the most attractive option by far: it had the highest per capita level of spending on cosmetics and toiletries of any country in the world, disposable income was high, it already had a thriving direct marketing industry, and it had a high proportion of women who did not participate in the work force. MKC learned, however, after participating in both markets, that the market opportunity in China was far greater, mainly because of economic and cultural distance: Chinese women were far more motivated than their Japanese counterparts to boost their income by becoming beauty consultants. Thus, the entrepreneurial opportunity represented by what MKC describes as “the career” (i.e., becoming a beauty consultant) was a far better predictor of the true sales potential than high-level data on incomes and expenditures. As a result of this experience, MKC now employs an additional business-specific indicator of market potential within its market assessment framework: the average wage for a female secretary in a country.Arnold (2004), p. 34.

MKC’s experience underscores the importance of analyzing distance. It also highlights the fact that different product markets have different success factors: some are brand-sensitive while pricing or intensive distribution are key to success in others. Country-level economic or demographic data do not provide much help in analyzing such issues; only locally gathered marketing intelligence can provide true indications of a market’s potential size and growth rate and its key success factors.

Minicase: Tata Making Inroads Into ChinaChow (2008, April 28).

Not content with just India, Mumbai-based Tata Group, the maker of the $2,500 Nano small car, is developing a small car for China. The platform is being designed and developed by a joint Indian and Chinese team based in China. The alliance won a new project for the complete design and development of a vehicle platform for a leading original equipment manufacturer for a small car for the China’s domestic market. The team is integrating components in automotive modules to radically improve manufacturability and bring down total cost.

Meanwhile, in 2009, Nanjing Tata AutoComp Systems began supplying automotive interior products to Shanghai General Motors and Changan Ford Automobile Company Products, including plastic vents, outlet parts, and cabin air-ventilation grilles. In the same year, Nanjing Tata began supplying General Motors Corporation in Europe. Eventually, the plant will supply global automakers in North America and Europe as well as emerging markets such as China.

Nanjing Auto is a wholly owned subsidiary of Tata AutoComp Systems, which is the automotive part manufacturing arm of India’s Tata Motors. The company has 30 manufacturing facilities, mainly in India, and production capabilities in automotive plastics and engineering. It also has 15 joint ventures with Tier 1 supplier companies, mainly in India.

The company has almost completed construction of the 280,000-square-foot Nanjing plant at a cost of approximately $15 million. The first phase included capacity to make parts for air vents, handles, cupholders, ashtrays, glove boxes, and floor consoles. When completed, the plant will have double the current capacity and will also produce instrument panels, door panels, and larger parts. The plant is operated by local Chinese employees; only a few managers are Indian.

In its bid to become a $1 billion global automotive supplier by 2008, Tata AutoComp had to expand into China. Total passenger car sales in India in 2007 were slightly more than 1.4 million units; in China, the number was more than 5.2 million units, according to data from Automotive Resources Asia, a division of J.D. Power and Associates. Tata Motors sold 221,256 passenger cars in India in 2007. In the same year, Shanghai General Motors sold 495,405 cars. “We see huge potential in China. To us, China is not just a manufacturing base, but a window to the global market. Our investments are keeping this promising future in mind,’” says the Tata AutoComp’s chief executive officer.

5.3 Entry Strategies: Modes of Entry

What is the best way to enter a new market? Should a company first establish an export base or license its products to gain experience in a newly targeted country or region? Or does the potential associated with first-mover status justify a bolder move such as entering an alliance, making an acquisition, or even starting a new subsidiary? Many companies move from exporting to licensing to a higher investment strategy, in effect treating these choices as a learning curve. Each has distinct advantages and disadvantages.

ExportingThe marketing and direct sale of domestically produced goods in another country. is the marketing and direct sale of domestically produced goods in another country. Exporting is a traditional and well-established method of reaching foreign markets. Since it does not require that the goods be produced in the target country, no investment in foreign production facilities is required. Most of the costs associated with exporting take the form of marketing expenses.

While relatively low risk, exporting entails substantial costs and limited control. Exporters typically have little control over the marketing and distribution of their products, face high transportation charges and possible tariffs, and must pay distributors for a variety of services. What is more, exporting does not give a company firsthand experience in staking out a competitive position abroad, and it makes it difficult to customize products and services to local tastes and preferences.

LicensingPermits a firm (licensee) in the target country to use the intangible property of the licensor for a fee. essentially permits a company in the target country to use the property of the licensor. Such property is usually intangible, such as trademarks, patents, and production techniques. The licensee pays a fee in exchange for the rights to use the intangible property and possibly for technical assistance as well.

Because little investment on the part of the licensor is required, licensing has the potential to provide a very large return on investment. However, because the licensee produces and markets the product, potential returns from manufacturing and marketing activities may be lost. Thus, licensing reduces cost and involves limited risk. However, it does not mitigate the substantial disadvantages associated with operating from a distance. As a rule, licensing strategies inhibit control and produce only moderate returns.

Strategic alliancesMethods by which firms share the resources and risks required to enter international markets. and joint venturesMethods by which firms share the resources and risks required to enter international markets. have become increasingly popular in recent years. They allow companies to share the risks and resources required to enter international markets. And although returns also may have to be shared, they give a company a degree of flexibility not afforded by going it alone through direct investment.

There are several motivations for companies to consider a partnership as they expand globally, including (a) facilitating market entry, (b) risk and reward sharing, (c) technology sharing, (d) joint product development, and (e) conforming to government regulations. Other benefits include political connections and distribution channel access that may depend on relationships.

Such alliances often are favorable when (a) the partners’ strategic goals converge while their competitive goals diverge; (b) the partners’ size, market power, and resources are small compared to the industry leaders; and (c) partners are able to learn from one another while limiting access to their own proprietary skills.

The key issues to consider in a joint venture are ownership, control, length of agreement, pricing, technology transfer, local firm capabilities and resources, and government intentions. Potential problems include (a) conflict over asymmetric new investments, (b) mistrust over proprietary knowledge, (c) performance ambiguity, that is, how to “split the pie,” (d) lack of parent firm support, (e) cultural clashes, and (f) if, how, and when to terminate the relationship.

Ultimately, most companies will aim at building their own presence through company-owned facilities in important international markets. Acquisitions or greenfield start-upsWholly-owned subsidiaries created by firms to gain entry in foreign markets. represent this ultimate commitment. Acquisition is faster, but starting a new, wholly owned subsidiary might be the preferred option if no suitable acquisition candidates can be found.

Also known as foreign direct investment (FDI)A firm’s direct ownership of facilities in a target country market., acquisitions and greenfield start-ups involve the direct ownership of facilities in the target country and, therefore, the transfer of resources including capital, technology, and personnel. Direct ownership provides a high degree of control in the operations and the ability to better know the consumers and competitive environment. However, it requires a high level of resources and a high degree of commitment.

Minicase: Coca-Cola and Illycafféhttp://www.thecoca-colacompany.com/; http://www.illy.com/

In March 2008, the Coca-Cola company and Illycaffé Spa finalized a joint venture and launched a premium ready-to-drink espresso-based coffee beverage. The joint venture, Ilko Coffee International, was created to bring three ready-to-drink coffee products—Caffè, an Italian chilled espresso-based coffee; Cappuccino, an intense espresso, blended with milk and dark cacao; and Latte Macchiato, a smooth espresso, swirled with milk—to consumers in 10 European countries. The products will be available in stylish, premium cans (150 ml for Caffè and 200 ml for the milk variants). All three offerings will be available in 10 European Coca-Cola Hellenic markets including Austria, Croatia, Greece, and Ukraine. Additional countries in Europe, Asia, North America, Eurasia, and the Pacific were slated for expansion into 2009.

The Coca-Cola Company is the world’s largest beverage company. Along with Coca-Cola, recognized as the world’s most valuable brand, the company markets four of the world’s top five nonalcoholic sparkling brands, including Diet Coke, Fanta, Sprite, and a wide range of other beverages, including diet and light beverages, waters, juices and juice drinks, teas, coffees, and energy and sports drinks. Through the world’s largest beverage distribution system, consumers in more than 200 countries enjoy the company’s beverages at a rate of 1.5 billion servings each day.

Based in Trieste, Italy, Illycaffé produces and markets a unique blend of espresso coffee under a single brand leader in quality. Over 6 million cups of Illy espresso coffee are enjoyed every day. Illy is sold in over 140 countries around the world and is available in more than 50,000 of the best restaurants and coffee bars. Illy buys green coffee directly from the growers of the highest quality Arabica through partnerships based on the mutual creation of value. The Trieste-based company fosters long-term collaborations with the world’s best coffee growers—in Brazil, Central America, India, and Africa—providing know-how and technology and offering above-market prices.

5.4 Entry Strategies: Timing

In addition to selecting the right mode of entry, the timing of entry is critical. Just as many companies have overestimated market potential abroad and underestimated the time and effort needed to create a real market presence, so have they justified their overseas’ expansion on the grounds of an urgent need to participate in the market early. Arguing that there existed a limited window of opportunity in which to act, which would reward only those players bold enough to move early, many companies made sizable commitments to foreign markets even though their own financial projections showed they would not be profitable for years to come. This dogmatic belief in the concept of a first-mover advantage (sometimes referred to as “pioneer advantage”) became one of the most widely established theories of business. It holds that the first entrant in a new market enjoys a unique advantage that later competitors cannot overcome (i.e., that the competitive advantage so obtained is structural and therefore sustainable).

Some companies have found this to be true. Procter & Gamble (P&G), for example, has always trailed rivals such as Unilever in certain large markets, including India and some Latin American countries, and the most obvious explanation is that its European rivals were participating in these countries long before P&G entered. Given that history, it is understandable that P&G erred on the side of urgency in reacting to the opening of large markets such as Russia and China. For many other companies, however, the concept of pioneer advantage was little more than an article of faith and was applied indiscriminately and with disastrous results to country-market entry, to product-market entry, and, in particular, to the “new economy” opportunities created by the Internet.

The “get in early” philosophy of pioneer advantage remains popular. And while there are clear examples of its successful application—the advantages gained by European companies from being early in “colonial” markets provide some evidence of pioneer advantage—first-mover advantage is overrated as a strategic principle. In fact, in many instances, there are disadvantages to being first. First, if there is no real first-mover advantage, being first often results in poor business performance, as the large number of companies that rushed into Russia and China attests to. Second, pioneers may not always be able to recoup their investment in marketing required to “kick start” the new market. When that happens, a “fast followerA firm that uses the benefits from prior market development by a pioneering firm to achieve profitability more quickly.” can benefit from the market development funded by the pioneer and leapfrog into earlier profitability.For a more detailed discussion, see Tellis, Golder, and Christensen (2001).

This ability of later entrants to free-ride on the pioneer’s market development investment is the most common source of first-mover disadvantage and suggests two critical conditions necessary for real first-mover advantage to exist. First, there must be a scarce resource in the market that the first entrant can acquire. Second, the first mover must be able to lock up that scarce resource in such a way that it creates a barrier to entry for potential competitors. A good example is provided by markets in which it is necessary for foreign firms to obtain a government permit or license to sell their products. In such cases, the license, and perhaps government approval, more generally, may be a scarce resource that will not be granted to all comers. The second condition is also necessary for first-mover advantage to develop. Many companies believed that brand preference created by being first constituted a valid source of first-mover advantage, only to find that, in most cases, consumers consider the alternatives available at the time of their first purchase, not which came first.

Minicase: Starbucks’ Global ExpansionStarbucks: A Global Work-in-Process (2006); http://www.starbucks.com/.

Starbucks’ decision to expand abroad came after an extended period of exclusive focus on the North American market. From its founding in 1971, it grew to almost 700 stores by 1995, all within the United States and Vancouver, Canada. It was not until the next decade that Starbucks made its first entry into international markets. By 2006, Starbucks operated approximately 11,000 stores, with 70% in the United States and 30% in international markets, and international revenue had grown to almost 20% of Starbucks’ total revenue. Starbucks offered the same basic coffee menu internationally as it did in the United States; however, the range of food products and other items, such as coffee mugs stocked, varied somewhat according to local customs and tastes.

Along with many other companies that pursue global expansion, Starbucks continually faces questions about where and how to further increase its global presence. Should the emphasis be on growth in existing countries or on increasing the number of countries in which it has a presence? How important is the fact that international markets so far have proven less profitable than the U.S. and Canadian markets?

Starbucks in Japan. Interestingly, Starbucks’ first foreign move (i.e., outside the United States and Canada) was a joint venture in Japan. At the time, Japan had the second largest economy in the world and was consistently among the top five coffee importers in the world.

The decision to use a joint venture to enter Japan followed intense internal debate. Concerns among senior executives centered on Starbucks’ lack of local knowledge, and questions were raised about the company’s ability to attract the local talent necessary to grow the Japanese business quickly enough. Starbucks was acutely aware that there were significant differences between doing business in Japan and in the United States and that it might not have enough experience to be successful on its own.

Among other factors, operating costs were predicted to be double those of North America, and Starbucks would have to pay to ship coffee to Japan from its roasting facility in Kent, Washington (near Seattle). In addition, retail space in Tokyo was 2 to 3 times as expensive as in Seattle. Just finding rental space in such a populous city might prove to be a tremendous challenge. Starbucks concluded it needed to form an alliance with a local group that had experience with complex operations and real estate.

Starbucks executives worried that a licensing deal would not be the right solution. Specifically, they were concerned about possible loss of control and insufficient knowledge transfer to learn from the experience. A joint venture was thought to be a better answer, and, after a long search, Starbucks approached Sazaby, Inc., operators of upscale retail and restaurant chains, whose president had approached Starbucks years earlier about the potential of opening Starbucks stores in Japan. Similarity in values, culture, and community-development goals between Starbucks and Sazaby were important considerations in concluding the 50-50 deal. The two companies were equally represented on the board of directors of the newly created Starbucks Coffee Japan. Starbucks was the sole decision-making power in matters relating to brand, product line advertising, and corporate communications, while decisions regarding real-estate operational issues and human resources were handled by Sazaby. Despite strong local competition, the venture was successful from the start. By fiscal year 2000, Starbucks Coffee Japan became profitable more than 2 years ahead of plan.

Starbucks in the United Kingdom. Unlike its expansion into Asia and (later) the Middle East, Starbucks chose to enter the United Kingdom through acquisition rather than partnerships. Speed was a major factor in Starbucks’ decision to enter the fast-growing UK market by acquisition. In addition, the culture, language, legal environment, management practices, and labor economics in the United Kingdom were considered sufficiently similar to those that Starbucks’ management already knew. This meant that a 100%-owned UK subsidiary could be successfully established from the outset. In May 1998, Starbucks acquired the Seattle Coffee Company, which had a presence in the United Kingdom for some time. This fast-growing chain was modeled on its own style of operations and, at the time of the purchase, had 56 retail units. The Seattle Coffee Company was an attractive acquisition target because of its focus: relatively small market capitalization and established retail units. By 2005, Starbucks had 469 stores in the United Kingdom, which made it the third largest country, after the United States and Japan, to serve Starbucks coffee.

Licensing in China. In a number of developing markets, including China, Starbucks chose to enter into minority share licensing agreements with high-quality, experienced local partners in order to minimize market-entry risks. Under these agreements, the local partners absorbed the capital costs (real estate, store construction) of bringing the Starbucks brand abroad. This eliminated the need for substantial general and administrative expenses by Starbucks and enabled it to establish a presence in foreign markets much more quickly than it would have if it had to invest its own capital and absorb start-up losses.

Risk was also a major consideration when Starbucks looked to enter China. While offering high-volume opportunities in an untapped coffee market, the prevailing culture and politics in China potentially posed significant problems. In April 2000, Beijing city authorities ordered Kentucky Fried Chicken to close its store near the Forbidden City when its lease expired in 2002. Similarly, under pressure from local authorities, McDonald’s removed its golden arches from outlets near Tiananmen Square. These incidents demonstrated China’s ambiguous attitude toward a growing Western economic and cultural influence.

Another major concern with starting operations in China was recruiting the right staff. Uniformity of customer experience and coffee quality was the key driver behind the Starbucks brand; failure to recruit the staff to ensure these key criteria not only would mean failure for the Chinese retail outlets but also could harm the company’s image globally.

Although these factors made licensing an attractive entry model, with growing experience in the Chinese market, Starbucks is steadily reducing its reliance on the licensing model and switching to its core company-operated business model to increase control and reap greater rewards.

Starbucks’ globalization history shows that while it was a “first mover” in the United States, it was forced to push harder in international markets to compete with existing players. In Japan, Starbucks was initially a huge success and became profitable 2 years earlier than anticipated. However, just 2 years after Starbucks Japan had become profitable, the company announced a loss of $3.9 million in Japan, its second largest market at the time, reflecting a major increase in local competition. Additional international challenges were a result of Starbucks’ chosen entry mode. Although joint ventures provided Starbucks with local knowledge about the market and a low-risk entry into unproven territory, joint ventures did not always reap the rewards that the partners had anticipated. One key factor was that it was often difficult for Starbucks to control the costs in a joint venture, resulting in lower profitability.

5.5 Points to Remember

- Selecting global target markets, entry modes, and deciding how much to adapt the company’s basic value proposition are intimately related. The choice of customers to serve in a particular country or region with a particular culture determines how and how much a company must adapt its basic value proposition. Conversely, the extent of a company’s capabilities in tailoring its offerings around the globe limits or broadens its options to successfully enter new markets or cultures.

- Few companies can afford to enter all markets open to them. The track record shows that picking the most attractive foreign markets, determining the best time to enter them, and selecting the right partners and level of investment has proven difficult for many companies, especially when it involves large emerging markets such as China.

- Research shows there is a pervasive the-grass-is-always-greener effect that infects global strategic decision making in many, especially globally inexperienced, companies and causes them to overestimate the attractiveness of foreign markets.

- Four key factors in selecting global markets are (a) a market’s size and growth rate, (b) a particular country or region’s institutional contexts, (c) a region’s competitive environment, and (d) a market’s cultural, administrative, geographic, and economic distance from other markets the company serves.

- There is a wide menu of options regarding market entry, from conservative strategies such as first establishing an export base or licensing products to gain experience in a newly targeted country to more aggressive options such as entering an alliance, making an acquisition, or even starting a new subsidiary.

- Selecting the right timing of entry is equally critical. And just as many companies have overestimated market potential abroad, and underestimated the time and effort needed to create a real market presence, so have they justified their overseas’ expansion on the grounds of an urgent need to participate in the market early.