This is “Cash Conversion Cycle”, section 17.3 from the book Finance for Managers (v. 0.1). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

17.3 Cash Conversion Cycle

PLEASE NOTE: This book is currently in draft form; material is not final.

Learning Objectives

- Describe the parts of the cash conversion cycle.

- Calculate the cash conversion cycle.

- Explain how to manage the cash conversion cycle to manage operating capital.

Central to a firm’s working capital management is an understanding of its cash conversion cycleThe length of time it takes a company to convert purchases of raw materials into cash received., or how long it takes for the company to convert cash invested in operations into cash received. The cash conversion cycle measures the time passed from the beginning of the production process to collection of cash from the sale of the finished product. Typically a firm buys raw materials and produces a product. This product goes into inventory and then is sold. Once the product is sold then the firm waits to recieve payment, at which point the process begins again. How long does this take? Understanding this cycle is essential to successful working capital management.

Calculating the Cash Conversion Cycle

The cash conversion cycle is divided into three parts: the average payment period, the average collection period and the average age of inventory. The firm’s operating cycleThe time from the receipt of raw materials until the receipt of cash for the sale of the goods. is length of time from the receipt of raw materials to the collection of payment for the goods sold. This is, essentially, how long it takes from the start of making a new product until we receive cash (on average). The operating cycle is thus the sum of the inventory conversion periodThe average time between when raw materials are received into inventory and product is sold. (the average time between when raw materials are received into inventory and product is sold) and the receivables conversion periodThe average time between a sale and collection of the receipt. (the average time between a sale and collection of the receipt).

Figure 17.4 Cash Conversion Cycle

The inventory conversion period can be estimated if we know the average balance of our inventory and the average value of goods sold each day of the year. The latter should be equal to cost of goods sold for the year divided by 365.

Equation 17.1 Inventory Conversion Period

As an example, if we have $60 thousand in inventory and sell $3 thousand worth of goods every day, then our inventory takes, on average, $60 thousand/$3 thousand per day = 20 days to sell. This, of course, includes production time as well as time that inventory “sits on the shelves”.

Likewise, the receivables conversion period can be estimated if we know the average balance of our account receivables and the average revenues each day of the year. The latter should be equal to revenues for the year divided by 365.

Equation 17.2 Receivables Conversion Period

As an example, if we have $12 thousand in receivables and sell $4 thousand in revenues per day, then our receivables take, on average, $120 thousand/$4 thousand per day = 30 days to collect.

Equation 17.3 Operating Cycle

In our examples, the operating cycle is 20 days + 30 days = 50 days.

When we purchase raw materials, however, we don’t typically pay for them immediately. Just as we offer customers credit, our suppliers will usually provide opportunities for credit to us. Therefore, our cash is not tied up for the entire operating cycle, but just the time from when we finally have to pay for raw materials. This length of time or payables conversion periodThe average time between acquiring raw materials and payment for them. (the average time between acquiring raw materials and payment for them) is subtracted from the operating cycle to determine the entire cash conversion cycle. Unfortunately, total purchases are not readily available from the income statement, so we will often have to estimate them as a percentage of cost of goods sold.

Equation 17.4 Payables Conversion Period

As an example, if we have $30 thousand in payables and purchase $2 thousand in raw materials per day, then our payables take, on average, $30 thousand/$2 thousand per day = 15 days.

Equation 17.5 Cash Conversion Cycle

Our examples cash conversion cycle is thus 20 days + 30 days − 15 days = 35 days.

Figure 17.5 Cash Conversion Cycle Example

Typically, the shorter the cash conversion cycle, the better, as it means we are keeping our cash moving instead of having it tied up in Net Working Capital. There are other considerations, however. Perhaps, extending collections of receivables, for example, might entice more sales from our customers. Then we need to balance the benefits from the extra sales with the additional costs in Net Working Capital due to the lengthening cash conversion cycle.

CABS Example

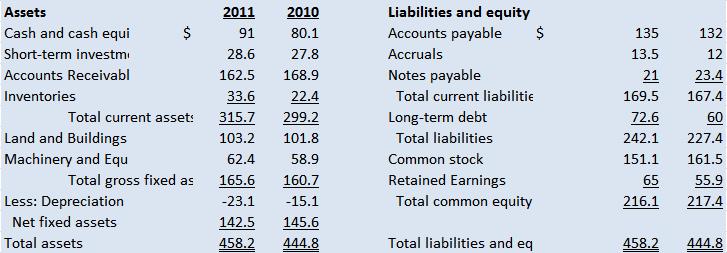

Figure 17.6 CABS Balance Sheet

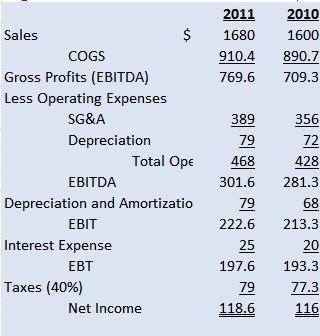

Figure 17.7 CABS Income Statement

Let’s calculate the cash conversion cycle for 2011. Let’s assume that purchases are 90% of the COGS.

First, need to determine the inventory conversion period. Average daily COGS is 910.4 thousand/365 days = 2.49 thousand per day. Ending inventory in 2011 was 33.6 thousand, so 33.6 thousand/2.49 thousand per day = 13.5 days.

What “average” should I take?

In this problem, we are using the ending balances as the average for inventory, A/R, and A/P. Another option would be to take the mean of the starting and end balances (that is, add them together and divide by 2). In reality, we need to use our best judgment as to what the appropriate representation for our company is.

Average daily revenues are 1,680 thousand/365 days = 4.60 thousand per day. Ending A/R in 2011 was 162.5 thousand, so 162.5 thousand/4.60 thousand per day = 35.3 days.

Annual purchases are 90% × 910.4 thousand = 819.4 thousand. Average daily purchases are 819.4 thousand/365 days = 2.24 thousand per day. Ending A/P in 2011 was 135 thousand, so 135 thousand/2.24 thousand per day = 60.3 days.

The cash conversion cycle is therefore 13.5 + 35.3 − 60.3 = −11.5 days. Since our payables conversion period is so long (almost twice the receivables conversion period), we end up paying for the materials after we’ve received payment from our customers!

How Do We Manage the Cash Conversion Cycle?

When a firm changes any of these variables, then their cash conversion cycle changes. Certain steps can be taken to reduce a firm’s cash conversion cycle. These steps include:

- Reduce the average age of inventory. Improve their inventory conversion period by making goods and selling them faster through more efficient processes. Avoiding inventory shortages or stockouts helps too.

- Reduce the average collection period. Speed up collections on accounts receivable. Collect A/R as quickly as possible without losing customers but maintain good credit relations with customers.

- Increase the payables deferral period. Pay A/P as slowly as possible without harming credit rating or relationship with supplier.

- Use technology, strategic partnerships and other leverages effectively. Use technology to collect payments, make product or any other use of technology which improves efficiency.

Key Takeaway

- The shorter the cash conversion cycle, the better we are managing our cash flow.

Exercises

- What does each of the components of the cash conversion cycle represent?

-

Calculate the cash conversion cycle given the following information:

Inventory Conversion Period = 25.3 days

Receivables Conversion Period = 19.9 days

Payables Conversion Period = 14.7 days