This is “Predictions and Effects”, section 5.3 from the book Finance, Banking, and Money (v. 2.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

5.3 Predictions and Effects

Learning Objective

- How does the interest rate react to changes in the money supply?

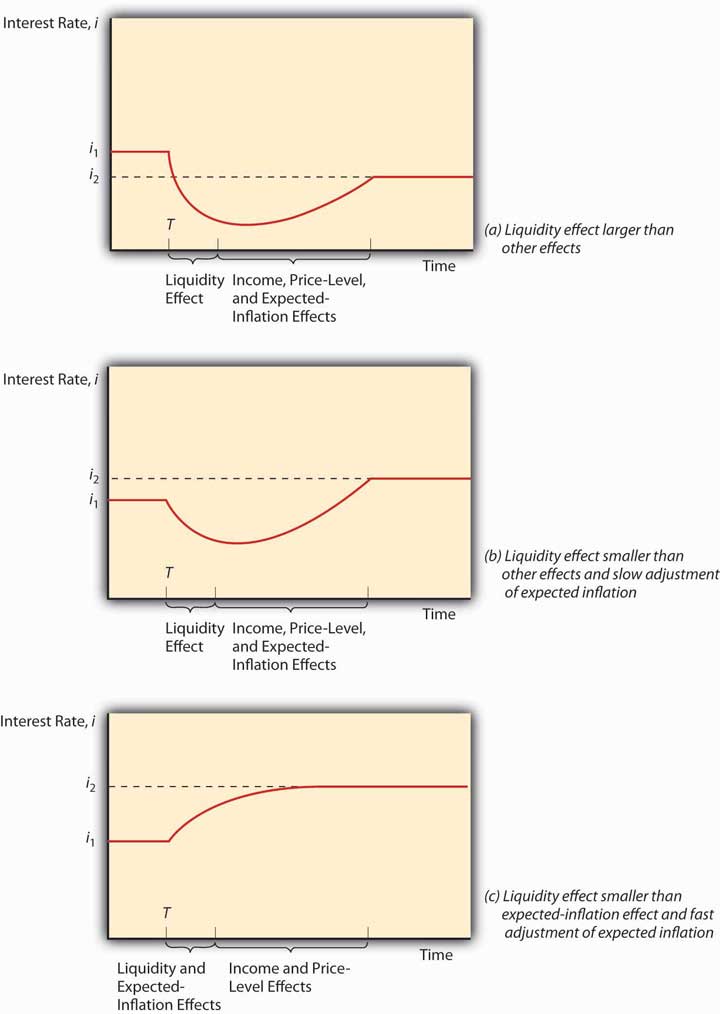

We’re almost there! At first blush, increasing the money supply would seem to decrease interest rates through what is called a liquidity effect: more money in circulation means more money to lend and hence, like more apples or carrots in a market, lower prices. Reality, however, is not so simple when it comes to the money supply. Government entities regulate the money supply and have a habit of expanding it because doing so prudently increases economic growth, employment, incomes, and other good stuff. Unfortunately, expanding the money supply also causes prices to rise almost every year, with no reversion to earlier levels. When the money supply increases, incomes rise, prices increase, and people expect inflation to occur. Each of those three effects, called the income, price level, and expected inflation effects, respectively, causes the interest rate to rise. Higher incomes mean more demand for bonds and higher prices, and expected inflation means bondholders need to receive a higher interest rate to offset losses in money’s purchasing power (the Fisher Effect). When the money supply increases, the liquidity effect, which lowers the interest rate, battles those three countervailing effects. Sometimes, the liquidity effect wins. When the money supply increases (or increases faster than usual), the liquidity effect overpowers the countervailing effects, and the interest rate declines and stays below the previous level. Sometimes, often in modern industrial economies with independent central banksA monetary authority that is controlled by public-interested technocrats rather than by self-interested politicians., the liquidity effect prevails at first and the interest rate declines, but then incomes rise, inflation expectations increase, and the price level actually rises, eventually causing the interest rate to increase above the original level. Finally, sometimes, as in modern undeveloped countries with weak central banking institutions, the expectation of inflation is so strong and so quick that it overwhelms the liquidity effect, driving up the interest rate immediately. Later, after incomes and the price level increase, the interest rate soars yet higher. Figure 5.10 "Money supply growth and nominal interest rates" summarizes this discussion graphically.

Figure 5.10 Money supply growth and nominal interest rates

Stop and Think Box

Famed monetary economist and Nobel laureate Milton Friedman was a staunch supporter of free markets and a critic of changes in the price level, particularly the rampant inflation of the 1970s. He argued that government monetary authorities ought to increase the money supply at some known, constant rate. If Friedman was so worried about price level changes, why didn’t he advocate permanently fixing the money supply (MS)?www.econlib.org/library/Enc/bios/Friedman.html

By fixing the MS, the interest rate would have risen higher and higher as the demand for money increased due to higher incomes and even simple population growth. Only deflation (decreases in the price level) could have countered that tendency, but deflation, Friedman knew, was as pernicious as inflation. A constant rate of MS growth, he believed, would keep the price level relatively stable and interest rate fluctuations less frequent or severe.

Key Takeaways

- Intuitively, an increase in the money supply decreases the interest rate and a decrease in the money supply increases it.

- Under a floating or fiat money system like we have today, an increase in the money supply might induce interest rates to rise immediately if inflation expectations were strong or to rise with a lag as actual inflation took place.