This is “Preparation of Financial Statements”, section 5.3 from the book Business Accounting (v. 2.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

5.3 Preparation of Financial Statements

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Prepare an income statement, statement of retained earnings, and balance sheet based on the balances in an adjusted trial balance.

- Explain the purpose and construction of closing entries.

Preparing Financial Statements

Question: The accounting process is clearly a series of defined steps that take a multitude of monetary transactions and eventually turn them into fairly presented financial statements. After all adjusting entries have been recorded in the journal and posted to the appropriate T-accounts in the ledger, what happens next in the accounting process?

Answer: After the adjusting entries are posted, the accountant should believe that all material misstatements have been removed from the accounts. Thus, they are presented fairly according to U.S. GAAP (or IFRS) and can be used by decision makers. As one final check, an adjusted trial balance is produced for a last, careful review. Assuming that no additional concerns are uncovered, the accountant prepares an income statement, a statement of retained earnings, and a balance sheet.

The basic financial statements are then completed by the production of a statement of cash flows. In contrast to the previous three, this statement does not report ending ledger account balances but rather discloses and organizes all of the changes that took place during the period in the composition of the cash account. As indicated in Chapter 3 "How Is Financial Information Delivered to Decision Makers Such as Investors and Creditors?", cash flows are classified as resulting from operating activities, investing activities, or financing activities.

The reporting process is then finalized by the preparation of explanatory notes that accompany a set of financial statements.

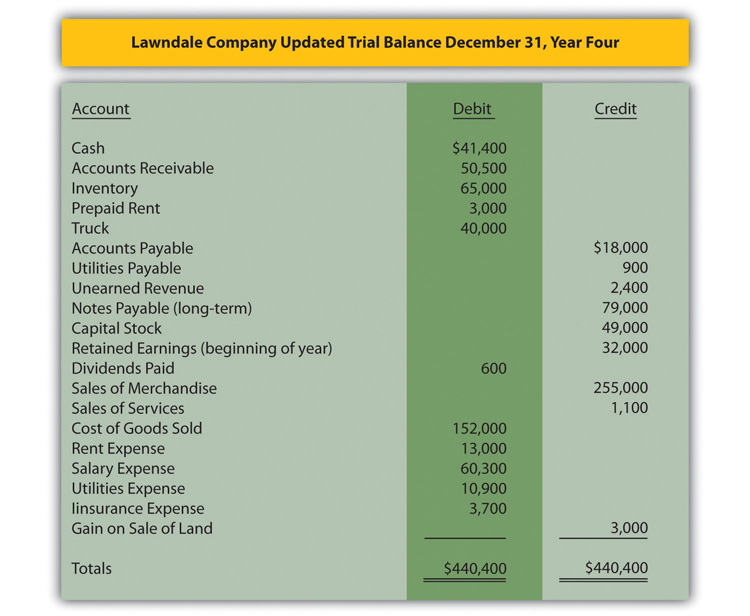

The final trial balance for the Lawndale Company (including the four adjusting entries produced earlier) is presented in Figure 5.7 "Updated Trial Balance for Lawndale Company—December 31, Year Four (after posting four adjusting entries to ". The original trial balance in Figure 5.1 "Updated Trial Balance for the Lawndale Company" has been updated by the four adjusting entries that were discussed in this chapter.

Adjusting Entry 1

- Utilities expense increases by $900

- Utilities payable increases by $900

Adjusting Entry 2 (Version 1)

- Rent expense increases by $1,000

- Prepaid rent decreases by $1,000

Adjusting Entry 3

- Accounts receivable increases by $500

- Sales of services increases by $500

Adjusting Entry 4

- Unearned revenue decreases by $600

- Sales of services increases by $600

These changes are entered into Figure 5.1 "Updated Trial Balance for the Lawndale Company" to bring about the totals presented in Figure 5.7 "Updated Trial Balance for Lawndale Company—December 31, Year Four (after posting four adjusting entries to ".

Figure 5.7 Updated Trial Balance for Lawndale Company—December 31, Year Four (after posting four adjusting entries to Figure 5.1 "Updated Trial Balance for the Lawndale Company")

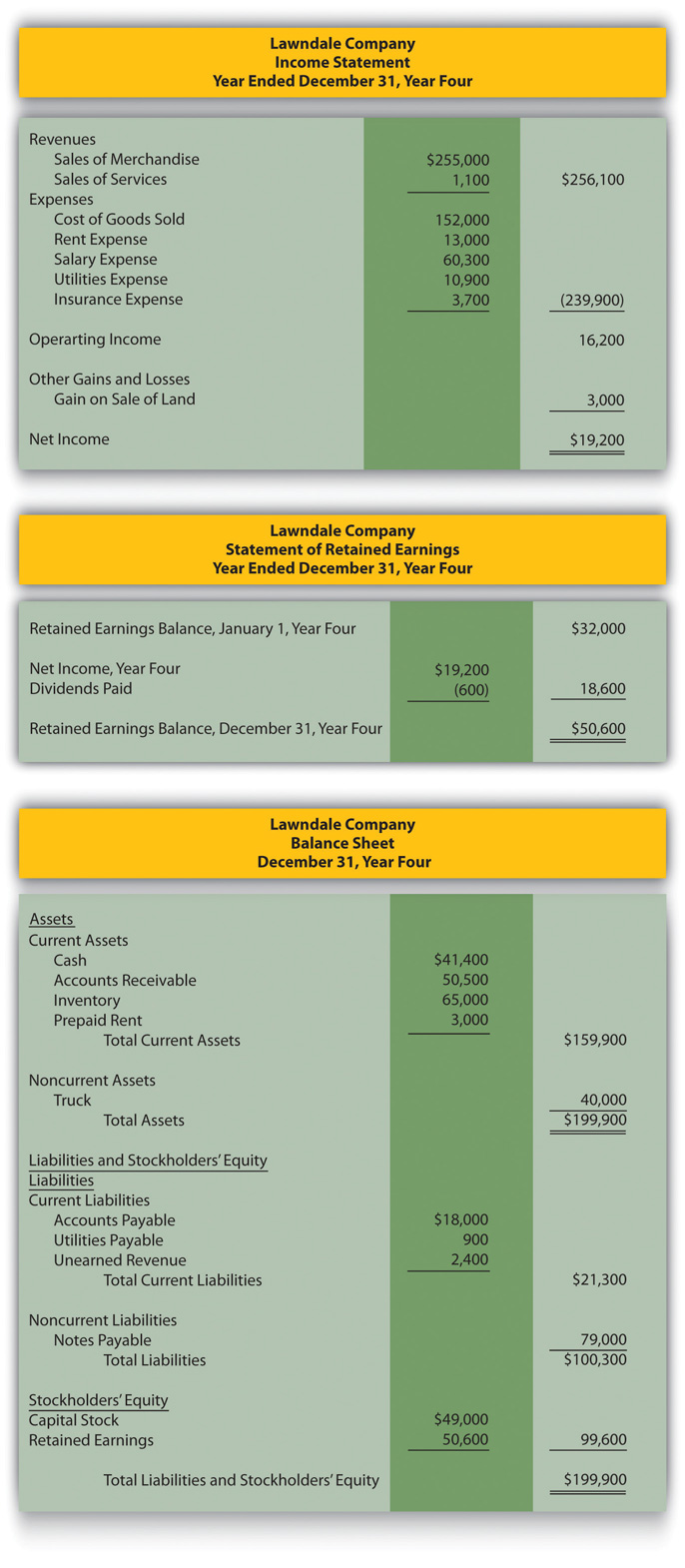

After that, each of the final figures is appropriately placed within the first three financial statements. Revenues and expenses appear in the income statement, assets and liabilities in the balance sheet, and so on. The resulting statements for the Lawndale Company are exhibited in Figure 5.8 "Year Four Financial Statements for Lawndale Company".

Figure 5.8 Year Four Financial Statements for Lawndale Company

To keep this initial illustration reasonably simple, no attempt has been made to record all possible accounts or adjusting entries. For example, no accrued expenses have been recognized for either income taxes or interest expense owed in connection with the notes payable. One example of an accrued expense is sufficient in this early coverage because both income taxes and interest expense will be described in depth in a later chapter. Likewise, depreciation expense of noncurrent assets with finite lives (such as the truck shown on the company’s trial balance) will be discussed subsequently. However, the creation of financial statements for the Lawndale Company should demonstrate the functioning of the accounting process as well as the basic structure of the income statement, statement of retained earnings, and balance sheet.

Several aspects of this process should be noted:

- The statements are properly identified by name of company, name of statement, and date. The balance sheet is for a particular day (December 31, Year Four) and the other statements cover a period of time (Year ending December 31, Year Four).

- Each account in the trial balance in Figure 5.7 "Updated Trial Balance for Lawndale Company—December 31, Year Four (after posting four adjusting entries to " appears within only one statement. Accounts receivable is an asset on the balance sheet. Cost of goods sold is an expense on the income statement. Dividends paid is a reduction shown on the statement of retained earnings. Each account serves one purpose and appears on only one financial statement.

- There is no T-account for net income. Net income is a composition of all revenues, gains, expenses, and losses for the year. The net income figure computed in the income statements is then used in the statement of retained earnings. In the same manner, there is no T-account for the ending retained earnings balance. Ending retained earnings is a composition of the beginning retained earnings balance, net income, and dividends paid. The ending retained earnings balance computed in the statement of retained earnings is then used in the balance sheet.

- The balance sheet does balance. The total of the assets is equal to the total of all liabilities and stockholders’ equity (capital stock and retained earnings). Assets must always have a source.

The statement of cash flows for the Lawndale Company cannot be created based solely on the limited information available in this chapter concerning the changes in the cash account. Thus, it has been omitted. Complete coverage of the preparation of a statement of cash flows will be presented in Chapter 17 "In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?".

The Purpose of Closing Entries

Question: Analyze, record, adjust, and report—the four basic steps in the accounting process. Is the work year complete for the accountant after financial statements are prepared?

Answer: One last mechanical process needs to be mentioned. Whether a business is as big as Microsoft or as small as the local convenience store, the final action performed each year by the accountant is the preparation of closing entriesEntries made to reduce all temporary ledger accounts (revenues, expenses, gains, losses, and dividends paid) to zero at the end of an accounting period so that a new measurement for the subsequent period can begin; the net effect of this process is transferred into the retained earnings account to update the beginning balance to the year-end figure.. Five types of accounts—revenues, expenses, gains, losses, and dividends paid—reflect the various increases and decreases that occur in a company’s net assets in the current period. These accounts are often deemed “temporary” because they only include changes for one year at a time. Consequently, the figure reported by Microsoft as its revenue for the year ended June 30, 2011, measures only sales during that year. T-accounts for rent expense, insurance expense, and the like reflect just the current decreases in net assets.

In order for the accounting system to start measuring the effects for each new year, these specific T-accounts must all be returned to a zero balance after annual financial statements are produced. Consequently, all of the revenue T-accounts maintained by Microsoft show a total at the end of its fiscal year (June 30, 2011) of $69.9 billion but contain a zero balance at the start of the very next day.

- Final credit totals existing in every revenue and gain account are closed out by recording equal and off-setting debits.

- Likewise, ending debit balances for expenses, losses, and dividends paid require a credit entry of the same amount to return each of these T-accounts to zero.

After these accounts are closed at year’s end, the resulting single figure is the equivalent of net income reported for the year (revenues and gains less expenses and losses) reduced by any dividends paid. This net effect is recorded in the retained earnings T-account. The closing process effectively moves the balance for every revenue, expense, gain, loss, and dividend paid into retained earnings. In the same manner as journal entries and adjusting entries, closing entries are recorded initially in the journal and then posted to the ledger. As a result, the beginning retained earnings balance for the year is updated to arrive at the ending total reported on the balance sheet.

Assets, liabilities, capital stock, and retained earnings all start out each year with a balance that is the same as the ending figure reported on the previous balance sheet. Those accounts are permanent; they are not designed to report an impact occurring during the current year. In contrast, revenues, expenses, gains, losses, and dividends paid all begin the first day of each year with a zero balance—ready to record the events of this new period.

Key Takeaway

After all adjustments are prepared and recorded, an adjusted trial balance is created, and those figures are used to produce financial statements. The income statement is prepared first, followed by the statement of retained earnings and then the balance sheet. The statement of cash flows is constructed separately because its figures do not come from ending T-account balances. Net income is determined on the income statement and also reported on the statement of retained earnings. Ending retained earnings is computed there and carried over to provide a year-end figure for the balance sheet. Finally, closing entries are prepared for revenues, expenses, gains, losses, and dividends paid. Through this process, all of these T-accounts are returned to zero balances so that recording for the new year can begin. The various amounts in these temporary accounts are moved to retained earnings. In this way, the beginning retained earnings balance for the year is increased to equal the ending total reported on the company’s balance sheet.

Talking with a Real Investing Pro (Continued)

Following is a continuation of our interview with Kevin G. Burns.

Question: Large business organizations such as PepsiCo and IBM have millions of transactions to analyze, classify, and record so that they can produce financial statements. That has to be a relatively expensive process that produces no revenue for the company. From your experience in analyzing financial statements and investment opportunities, do you think companies should spend more money on their accounting systems or would they be wise to spend less and save their resources?

Kevin Burns: Given the situations of the last decade ranging from the accounting scandals of Enron and WorldCom to recent troubles in the major investment banks, the credibility of financial statements and financial officers has eroded significantly. My view is that—particularly today—transparency is absolutely paramount and the more detail the better. Along those lines, I think any amounts spent by corporate officials to increase transparency in their financial reporting, and therefore improve investor confidence, is money well spent.

Video Clip

(click to see video)Professor Joe Hoyle talks about the five most important points in Chapter 5 "Why Is Financial Information Adjusted Prior to the Production of Financial Statements?".