This is “Investments and Markets: A Brief Overview”, section 12.1 from the book Individual Finance (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

12.1 Investments and Markets: A Brief Overview

Learning Objectives

- Identify the features and uses of issuing, owning, and trading bonds.

- Identify the uses of issuing, owning, and trading stocks.

- Identify the features and uses of issuing, owning, and trading commodities and derivatives.

- Identify the features and uses of issuing, owning, and trading mutual funds, including exchange-traded funds and index funds.

- Describe the reasons for different instruments in different markets.

Before looking at investment planning and strategy, it is important to take a closer look at the galaxy of investments and markets where investing takes place. Understanding how markets work, how different investments work, and how different investors can use investments is critical to understanding how to begin to plan your investment goals and strategies.

You have looked at using the money markets to save surplus cash for the short term. Investing is primarily about using the capital markets to invest surplus cash for the longer term. As in the money markets, when you invest in the capital markets, you are selling liquidity.

The capital markets developed as a way for buyers to buy liquidity. In Western Europe, where many of our ideas of modern finance began, those early buyers were usually monarchs or members of the nobility, raising capital to finance armies and navies to conquer or defend territories or resources. Many devices and markets were used to raise capital,For a thorough history of the evolution of finance and financial instruments, see Charles P. Kindleberger, A Financial History of Western Europe (London: George Allen & Unwin, Ltd., 1984). but the two primary methods that have evolved into modern times are the bond and stock markets. (Both are discussed in greater detail in Chapter 15 "Owning Stocks" and Chapter 16 "Owning Bonds", but a brief introduction is provided here to give you the basic idea of what they are and how they can be used as investments.)

In the United States, 47 percent of the adult population owns stocks or bonds, most through retirement accounts.John Sabelhaus, Michael Bogdan, and Daniel Schrass, “Equity and Bond Ownership in America, 2008,” Investment Company Institute and Securities Industry and Financial Markets Association, http://www.ici.org/pdf/rpt_08_equity_owners.pdf (accessed on May 20, 2009).

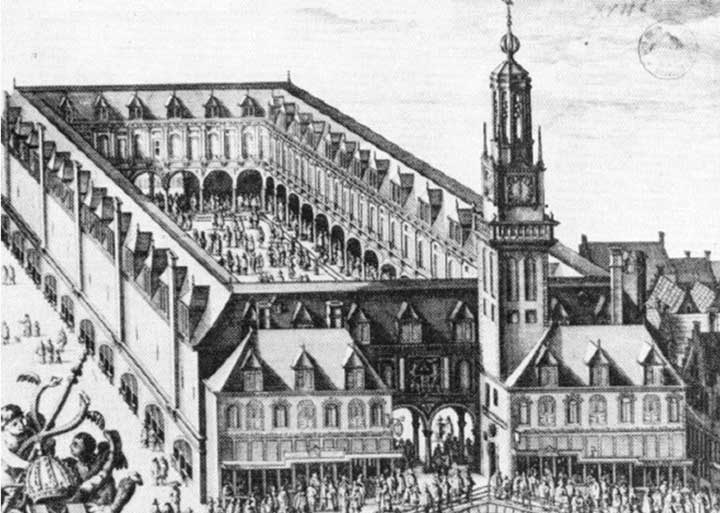

Figure 12.2 Amsterdam Stock Exchange

The Amsterdam Stock Exchange was established in 1602 by the Dutch East India Company, the first company in the world to issue stock and trade publicly. The company paid 18 percent annually for nearly two hundred years, based on its near monopoly of the Indonesian spice trade. Competition and corruption ended the exchange, which went bankrupt in 1798.

© Amsterdam Municipal Department for the Preservation and Restoration of Historic Buildings and Sites; used by permission.

Bonds and Bond Markets

BondsPublicly issued and traded long-term debt used by corporations and governments. are debt. The bond issuer borrows by selling a bond, promising the buyer regular interest payments and then repayment of the principal at maturity. If a company wants to borrow, it could just go to one lender and borrow. But if the company wants to borrow a lot, it may be difficult to find any one investor with the capital and the inclination to make large a loan, taking a large risk on only one borrower. In this case the company may need to find a lot of lenders who will each lend a little money, and this is done through selling bonds.

A bond is a formal contract to repay borrowed money with interest (often referred to as the coupon) at fixed intervals. Corporations and governments (e.g., federal, state, municipal, and foreign) borrow by issuing bonds. The interest rate on the bond may be a fixed interest rateA bond interest rate that does not change over time, from issuance to maturity. or a floating interest rateA bond interest rate that changes over time, usually related to a benchmark rate such as the U.S. discount rate or prime rate. that changes as underlying interest rates—rates on debt of comparable companies—change. (Underlying interest rates include the prime rate that banks charge their most trustworthy borrowers and the target rates set by the Federal Reserve Bank.)

There are many features of bonds other than the principal and interest, such as the issue priceThe original market price of a bond at issuance. (the price you pay to buy the bond when it is first issued) and the maturity dateDate at which a bond matures, or the end of the bond’s term, when the bond must be redeemed. (when the issuer of the bond has to repay you). Bonds may also be “callable”: redeemableA bond that is eligible for redemption. before maturityThe date on which payment of a financial obligation is due, such as bond redemption date. (paid off early). Bonds may also be issued with various covenantsA condition placed on bond issuers (borrowers) to protect bondholders (lenders). or conditions that the borrower must meet to protect the bondholders, the lenders. For example, the borrower, the bond issuer, may be required to keep a certain level of cash on hand, relative to its short-term debts, or may not be allowed to issue more debt until this bond is paid off.

Because of the diversity and flexibility of bond features, the bond markets are not as transparent as the stock markets; that is, the relationship between the bond and its price is harder to determine. The U.S. bond market is now more than twice the size (in dollars of capitalization) of all the U.S. stock exchanges combined, with debt of more than $27 trillion by the end of 2007.Financial Industry Regulatory Authority (FINRA), http://apps.finra.org/ (accessed May 20, 2009).

U.S. Treasury bonds are auctioned regularly to banks and large institutional investors by the Treasury Department, but individuals can buy U.S. Treasury bonds directly from the U.S. government (http://www.treasurydirect.gov). To trade any other kind of bond, you have to go through a broker. The brokerage firm acts as a principal or dealer, buying from or selling to investors, or as an agent for another buyer or seller.

Stocks and Stock Markets

StocksShares issued to account for ownership, as defined by owners’ contributions to a corporation. or equity securities are shares of ownership. When you buy a share of stock, you buy a share of the corporation. The size of your share of the corporation is proportional to the size of your stock holding. Since corporations exist to create profit for the owners, when you buy a share of the corporation, you buy a share of its future profits. You are literally sharing in the fortunes of the company.

Unlike bonds, however, shares do not promise you any returns at all. If the company does create a profit, some of that profit may be paid out to owners as a dividendA share of corporate profit distributed to shareholders, usually as cash or corporate stock., usually in cash but sometimes in additional shares of stock. The company may pay no dividend at all, however, in which case the value of your shares should rise as the company’s profits rise. But even if the company is profitable, the value of its shares may not rise, for a variety of reasons having to do more with the markets or the larger economy than with the company itself. Likewise, when you invest in stocks, you share the company’s losses, which may decrease the value of your shares.

Corporations issue shares to raise capital. When shares are issued and traded in a public market such as a stock exchangeAn organized market for the trading of corporate shares conducted by members of the exchange., the corporation is “publicly traded.” There are many stock exchanges in the United States and around the world. The two best known in the United States are the New York Stock Exchange (now NYSE Euronext), founded in 1792, and the NASDAQ, a computerized trading system managed by the National Association of Securities Dealers (the “AQ” stands for “Automated Quotations”).

Only members of an exchange may trade on the exchange, so to buy or sell stocks you must go through a broker who is a member of the exchange. Brokers also manage your account and offer varying levels of advice and access to research. Most brokers have Web-based trading systems. Some discount brokers offer minimal advice and research along with minimal trading commissions and fees.

Figure 12.3 Shanghai Stock Exchange, China

The Shanghai Stock Exchange (SSE), one of three exchanges in China, is not open to foreign investors. It is the sixth largest stock exchange in the world. The other exchanges in China are the Shenzhen Stock Exchange (SZSE) and the Hong Kong Stock Exchange (HKE). The Hang Seng is an index of Asian stocks on the HKE that is popular with investors interested in investing in Asian companies.

© Baycrest Gallery, used by permission

Commodities and Derivatives

CommoditiesRaw materials—natural resources or agricultural products—used as inputs in processing goods and services. are resources or raw materials, including the following:

- Agricultural products (food and fibers), such as soybeans, pork bellies, and cotton

- Energy resources such as oil, coal, and natural gas

- Precious metals such as gold, silver, and copper

- Currencies, such as the dollar, yen, and euro

Commodity trading was formalized because of the risks inherent in producing commodities—raising and harvesting agricultural products or natural resources—and the resulting volatility of commodity prices. As farming and food production became mechanized and required a larger investment of capital, commodity producers and users wanted a way to reduce volatility by locking in prices over the longer term.

The answer was futures and forward contracts. FuturesA publicly traded contract to buy or sell an asset at a specified time and price in the future. and forward contractsA private contract to buy or sell an asset at a specified time and price in the future. or forwards are a form of derivativesFinancial instruments such as options, futures, forwards, securitized assets, and so on whose value is derived from the value of another asset., the term for any financial instrument whose value is derived from the value of another security. For example, suppose it is now July 2010. If you know that you will want to have wheat in May of 2011, you could wait until May 2011 and buy the wheat at the market price, which is unknown in July 2010. Or you could buy it now, paying today’s price, and store the wheat until May 2011. Doing so would remove your future price uncertainty, but you would incur the cost of storing the wheat.

Alternatively, you could buy a futures contract for May 2011 wheat in July 2010. You would be buying May 2011 wheat at a price that is now known to you (as stated in the futures contract), but you will not take delivery of the wheat until May 2011. The value of the futures contract to you is that you are removing the future price uncertainty without incurring any storage costs. In July 2010 the value of a contract to buy May 2011 wheat depends on what the price of wheat actually turns out to be in May 2011.

Forward contracts are traded privately, as a direct deal made between the seller and the buyer, while futures contracts are traded publicly on an exchange such as the Chicago Mercantile Exchange (CME) or the New York Mercantile Exchange (NYMEX).

When you buy a forward contract for wheat, for example, you are literally buying future wheat, wheat that doesn’t yet exist. Buying it now, you avoid any uncertainty about the price, which may change. Likewise, by writing a contract to sell future wheat, you lock in a price for your crop or a return for your investment in seed and fertilizer.

Futures and forward contracts proved so successful in shielding against some risk that they are now written for many more types of “commodities,” such as interest rates and stock market indices. More kinds of derivatives have been created as well, such as options. OptionsThe right but not the obligation to buy or sell at a specific price at a specific time in the future; commonly written on shares of stock as well as on stock indices, interest rates, and commodities. are the right but not the obligation to buy or sell at a specific price at a specific time in the future. Options are commonly written on shares of stock as well as on stock indices, interest rates, and commodities.

Derivatives such as forwards, futures, and options are used to hedge or protect against an existing risk or to speculate on a future price. For a number of reasons, commodities and derivatives are more risky than investing in stocks and bonds and are not the best choice for most individual investors.

Mutual Funds, Index Funds, and Exchange-Traded Funds

A mutual fundA portfolio of investments created by an investment company such as a brokerage or bank. It is financed as the investment company sells shares of the fund to investors. For investors, a mutual fund provides a way to achieve maximum diversification with minimal transaction costs through economies of scale. is an investment portfolio consisting of securities that an individual investor can invest in all at once without having to buy each investment individually. The fund thus allows you to own the performance of many investments while actually buying—and paying the transaction cost for buying—only one investment.

Mutual funds have become popular because they can provide diverse investments with a minimum of transaction costs. In theory, they also provide good returns through the performance of professional portfolio managers.

An index fundA mutual fund designed to track the performance of an index for investors who seek diversification without having to select securities. is a mutual fund designed to mimic the performance of an index, a particular collection of stocks or bonds whose performance is tracked as an indicator of the performance of an entire class or type of security. For example, the Standard & Poor’s (S&P) 500 is an index of the five hundred largest publicly traded corporations, and the famous Dow Jones Industrial Average is an index of thirty stocks of major industrial corporations. An index fund is a mutual fund invested in the same securities as the index and so requires minimal management and should have minimal management fees or costs.

Mutual funds are created and managed by mutual fund companies or by brokerages or even banks. To trade shares of a mutual fund you must have an account with the company, brokerage, or bank. Mutual funds are a large component of individual retirement accounts and of defined contribution plans.

Mutual fund shares are valued at the close of trading each day and orders placed the next day are executed at that price until it closes. An exchange-traded fund (ETF)A fund that tracks an index or a commodity or a basket of assets but is traded like stocks on a stock exchange. is a mutual fund that trades like a share of stock in that it is valued continuously throughout the day, and trades are executed at the market price.

The ways that capital can be bought and sold is limited only by the imagination. When corporations or governments need financing, they invent ways to entice investors and promise them a return. The last thirty years has seen an explosion in financial engineeringThe use of mathematical modeling to create and value new financial instruments and markets., the innovation of new financial instruments through mathematical pricing models. This explosion has coincided with the ever-expanding powers of the computer, allowing professional investors to run the millions of calculations involved in sophisticated pricing models. The Internet also gives amateurs instantaneous access to information and accounts.

Much of the modern portfolio theory that spawned these innovations (i.e., the idea of using the predictability of returns to manage portfolios of investments) is based on an infinite time horizon, looking at performance over very long periods of time. This has been very valuable for institutional investors (e.g., pension funds, insurance companies, endowments, foundations, and trusts) as it gives them the chance to magnify returns over their infinite horizons.

Figure 12.4

© 2010 Jupiterimages Corporation

For most individual investors, however, most portfolio theory may present too much risk or just be impractical. Individual investors don’t have an infinite time horizon. You have only a comparatively small amount of time to create wealth and to enjoy it. For individual investors, investing is a process of balancing the demands and desires of returns with the costs of risk, before time runs out.

Key Takeaways

-

Bonds are

- a way to raise capital through borrowing, used by corporations and governments;

- an investment for the bondholder that creates return through regular, fixed or floating interest payments on the debt and the repayment of principal at maturity;

- traded on bond exchanges through brokers.

-

Stocks are

- a way to raise capital through selling ownership or equity;

- an investment for shareholders that creates return through the distribution of corporate profits as dividends or through gains (losses) in corporate value;

- traded on stock exchanges through member brokers.

-

Commodities are

- natural or cultivated resources;

- traded to hedge revenue or production needs or to speculate on resources’ prices;

- traded on commodities exchanges through brokers.

- Derivatives are instruments based on the future, and therefore uncertain, price of another security, such as a share of stock, a government bond, a currency, or a commodity.

-

Mutual funds are portfolios of investments designed to achieve maximum diversification with minimal cost through economies of scale.

- An index fund is a mutual fund designed to replicate the performance of an asset class or selection of investments listed on an index.

- An exchange-traded fund is a mutual fund whose shares are traded on an exchange.

- Institutional and individual investors differ in the use of different investment instruments and in using them to create appropriate portfolios.

Exercises

- In My Notes or your personal finance journal, record your experiences with investing. What investments have you made, and how much do you have invested? What stocks, bonds, funds, or other instruments, described in this section, do you have now (or had in the past)? How were the decisions about your investments made, and who made them? If you have had no personal experience with investing, explain your reasons. What reasons might you have for investing (or not) in the future?

- About how many stock exchanges exist in the world? Which geographic region has the greatest number of exchanges? Sample features of stock exchanges on each continent at http://www.tdd.lt/slnews/Stock_Exchanges/Stock.Exchanges.htm. What characteristics do all the exchanges share?

- What is a brokerage house, and when would you use a broker? Find out at http://www.wisegeek.com/what-is-a-brokerage-house.htm. Sample brokerage houses that advertise online. What basic products and services do all brokerages offer? According to the advice at http://gti.cuna.org/18592/worksheets/evaluate_broker.pdf, what is the best way to choose a broker? Discuss brokers with classmates to develop a list of ten questions you would want to ask a broker before you opened an account. (Hint: Search the Motley Fool’s 2009 “Brokerage Questions for Beginners” at http://www.fool.com.)

- Visit the Chicago Mercantile Exchange at http://www.cmegroup.com/. What are some examples of commodities on the CME that theoretically could be part of your investment portfolio? In what energy product does the CME specialize? Could you invest in whether a foreign currency will rise or fall in relation to another currency? Could you invest in whether interest rates will rise or fall? Could you invest in how the weather will change?

- An example of financial engineering is the derivative known as the credit default swap, a form of insurance against defaults on underlying financial instruments—for example, paying out on defaults on loan payments. According to Senator Harkin’s (D-Iowa) 2009 report at http://www.iowapolitics.com/index.iml?Article=160768, why must derivatives like credit default swaps and their markets be more rigorously regulated? Regulation is a perennial political issue. What are some arguments for and against the regulation or deregulation of the capital markets? What are the implications of regulation and deregulation for investors?